Running on progressive platforms that include ending mass incarceration and addressing police misconduct, candidates defeated traditional “law-and-order” prosecutors across the country.

Elected prosecutors – often called state’s attorneys or district attorneys – represent the people of a particular county in their criminal cases. Their offices work with law enforcement to investigate and try cases, determine which crimes should be prioritized and decide how punitive to be.

After decades of incumbent prosecutors winning reelection based on their high conviction rates or the long sentences they achieved, advocates for criminal justice reform began making inroads into their territory a few years ago. They did so mainly by drawing attention to local races and funding progressive challengers.

Despite criticism during her first term, progressive prosecutor Kim Foxx won reelection as Cook County state’s attorney by a 14-point margin. Scott Olson/Getty Images

Birth of a movement

During her 2016 run for state’s attorney for Cook County, Illinois, Kim Foxx vowed to bring more accountability to police shootings and reduce prosecutions for nonviolent crimes.

She won, becoming the first Black woman to serve as state’s attorney in Chicago. It was also the first high-profile sign that this progressive prosecutorial approach was working.

Her victory was followed by the 2017 election of Larry Krasner as district attorney in Philadelphia. Krasner, a former civil rights attorney, had never prosecuted a case when he ran for office – a move that the city’s police union chief called “hilarious.”

But Krasner’s campaign platform – addressing mass incarceration and police misconduct – responded to a city saddled with the highest incarceration rate among large U.S. cities, nearly seven out of every 1,000 citizens. Krasner won with 75% of the vote.

As a criminal procedure professor and a former federal prosecutor, I have watched the desire for reform only grow since then.

Black Lives Matter protests have also focused attention on how prosecutors make decisions – whom they prosecute and how severely, particularly in police violence cases.

In Detroit, Karen McDonald won her race for Oakland County prosecutor by promising “common-sense criminal justice reform that utilizes treatment courts and diversion programs, addresses racial disparity, and creates a fair system for all people.”

“I think people are starting to realize, ‘Why don’t I know who my DA is?‘” said Gordon McLaughlin, the new district attorney for Colorado’s Eighth Judicial District, who campaigned on alternatives to incarceration for nonviolent offenders. “It’s brought criminal justice into the main conversation.”

Police accountability

One prominent issue on voters’ minds is how prosecutors’ offices choose to handle police violence.

George Gascón, candidate for Los Angeles district attorney, speaks during a drive-in election night watch party at the LA Zoo parking lot on Tuesday, Nov. 3, 2020.Myung J. Chun/Los Angeles Times via Getty Images

Gascón vowed to hold police accountable for officer-involved shootings. During the campaign, he pledged to reopen high-profile cases, including two where people were shot for not complying with an officer’s directions.

Mass incarceration and cash bail

Progressive prosecutors are likely to have the most impact by diverting people away from the criminal justice system in the first place.

Many have been motivated by what they see as “the criminalization of poverty” – a phenomenon in which the poor compile criminal records for minor offenses because they cannot afford bail or effective legal counsel.

Alonzo Payne, the new district attorney for San Luis Valley, Colorado, was outraged that poor people were forced to stay in jail because they couldn’t afford to post bond.

“I decided I wanted to bring some human compassion to the DA’s office,” he told the Denver Post.

Reforming the cash bail system and reducing mass incarceration is a goal shared by all of the newly elected prosecutors this election cycle, including Jose Garza, an immigrant rights attorney, in Austin, Texas.

Looking ahead

It seems that progressive policies are here to stay in some of the nation’s largest cities, but reformers didn’t enjoy success everywhere.

Candidates Zack Thomas in Johnson County, Kansas, and Julie Gunnigle in Maricopa County, Arizona, lost their races. And incumbents withstood reformist challengers in Cincinnati, Ohio, and Charleston, South Carolina.

Nonetheless, progressive prosecutors are increasingly winning races – and staying in power – by using the criminal justice system in more equitable ways.

Worrell, in Orlando, is a good example. She ran the Conviction Integrity Unit in the district attorney’s office, investigating innocence claims from convicted defendants.

Her reform message resonated a lot more with voters than the message of her opponent, Jose Torroella, who pledged to be “more old-fashioned” and more “strict.” Worrell won the race with nearly 66% of the votes.

“Criminal justice reform is not something people should be afraid of,” Worrell said. “It means we’re going to be smart on crime, rather than tough on crime.”

Republished with permission under license from The Conversation.

by Guo Xu, University of California, Berkeley and Abhay Aneja, University of California, Berkeley

Economic disparities in earnings, health and wealth between Black and white Americans are staggeringly large. Historical government practices and institutions – such as segregated schools, redlined neighborhoods and discrimination in medical care – have contributed to these wide disparities. While these causes may not always be overt, they can have lasting negative effects on the prosperity of minority communities.

Abhay Aneja and I are researchers at University of California, Berkeley, who specialize in examining the causes of social inequality. Our new research examines the U.S. federal government’s role in creating conditions of racial inequality more than a century ago. Specifically, we researched the harmful impact of government discrimination against Black civil service employees. We also examined how such discrimination continues to affect their families decades later, rippling across future generations.

A 1938 stamp honoring former President Woodrow Wilson, considered one of America’s most progressive presidents. iStock / Getty Images Plus

Decades of discrimination

Soon after his inauguration in 1913, President Woodrow Wilson ushered in one of the most far-reaching discrimination policies of that century. Wilson discreetly authorized his Cabinet secretaries to implement a policy of racial segregation across the federal bureaucracy.

A Southerner by heritage, Wilson appointed several Southern Democrats to Cabinet offices, several of whom were sympathetic to the segregationist cause. Wilson’s new postmaster general, for example, was “anxious to segregate white and negro employees in all Departments of Government.” Historical accounts suggest that Wilson’s order was carried out most aggressively by the U.S. Postal Service and the U.S. Treasury Department, the latter responsible for revenue generation including taxes and customs duties. Based on the data we collected, the majority of Black civilians worked in these two federal departments before Wilson’s arrival.

Given his support among Southern Democrats, one goal of the Wilson administration was to limit the access of Black civil servants to the highest positions within government. This outcome was achieved through both demotions and reductions, efforts to discourage the hiring of qualified Black candidates.

For example, photos became required to apply for government jobs in order to screen out Black candidates. Black Americans already employed in the federal civil service were transferred from relatively high-status posts to low-paying ones. This overall policy of Jim Crow-style segregation served to shut out Black Americans from working in one of the few places where they could find opportunities for economic mobility and success.

Deep roots of economic disparities

Despite the potential for enormous harm, the cost of segregation to the economic status of Black civil servants has long remained unknown. Our research started by examining how President Wilson contributed to earnings disparities between Black and white civil service workers. In so doing, our research added to the collective knowledge within the social sciences about the roots of racial inequality.

To build a database on earnings inequality, our team undertook a large-scale data digitization of previously undigitized and, to our knowledge, unexamined historical government records containing a detailed list of all people who worked for the federal government and what they earned each year. These records were contained in eight volumes of the Official Register of the U.S., a series spanning 1907 to 1921. For 1907, we obtained information for 125,000 workers. By 1921, the size of the government workforce had more than doubled.

This data collection and cleaning process created a comprehensive dataset to understand the operation of the American federal government at the beginning of the 20th century. It not only described a worker’s position and salary, but also contained rich personal information including a federal employee’s place of birth, the state from which they were appointed and the Cabinet department where they worked.

Because the register was issued every two years, our research made it possible to track a civil servant’s career progression over time. Looking at this data source, it was clear that President Wilson’s policy of segregating the federal workforce exacted an enormous cost from Black civil servants.

Sidelining Black federal workers

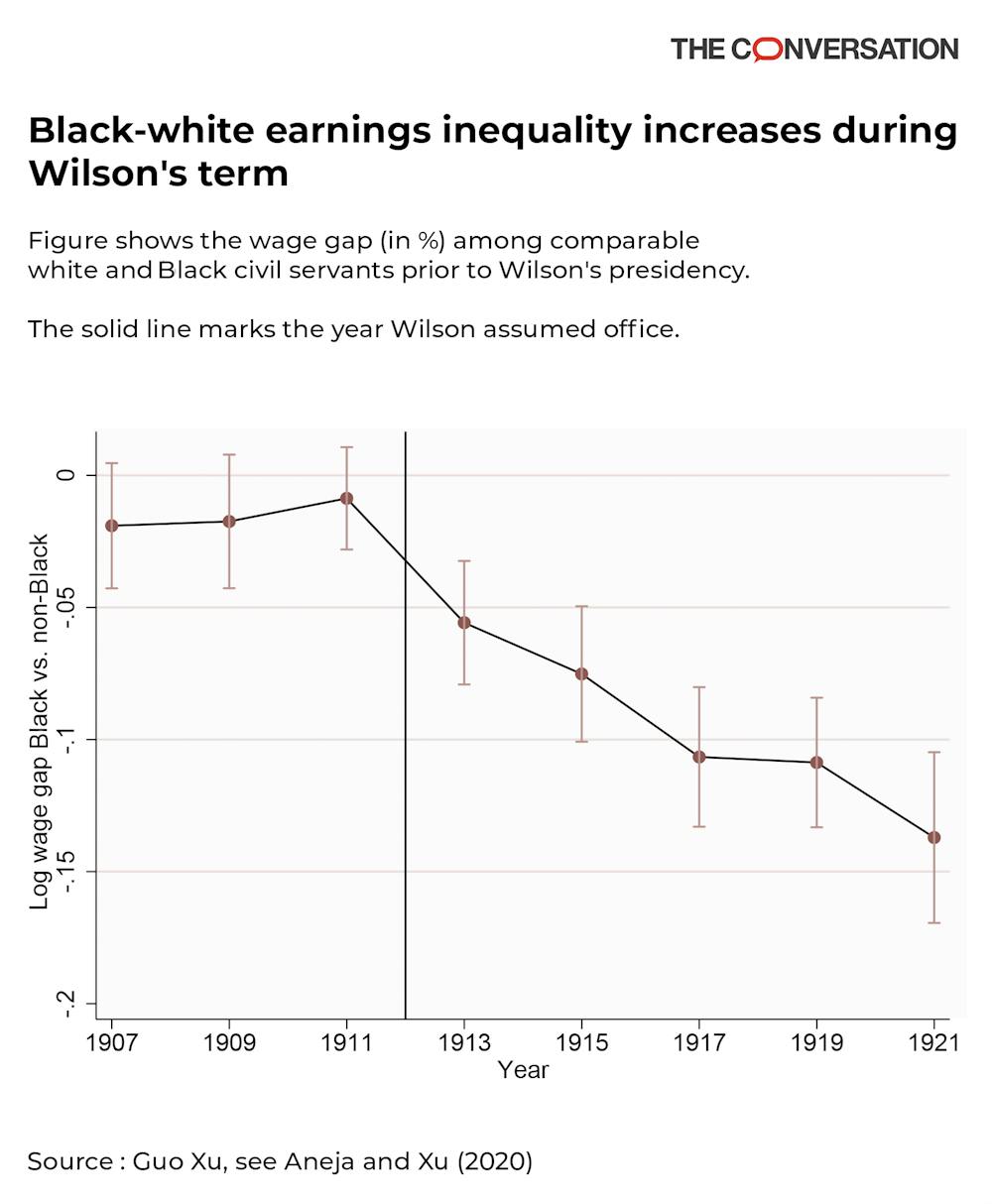

To isolate the impact of racial discrimination and establish comparable jobs and salaries, the analysis paired Black and white federal employees with similar characteristics. Each worked in the same city, the same government office and even had the same salary before President Wilson’s inauguration. Within this set of comparable workers, Black civil servants earned about 7% less than their white counterparts during Wilson’s two terms as president.

When we account for differences in civil servants, such as educational background, the reduction in earnings suffered by Black civil servants remains. Moreover, under the order to segregate, Black civil servants were less likely to be promoted over time and more likely to be demoted. This disparate treatment by the federal government enabled white civil servants to earn more over time than Black civil servants with the same levels of skill and experience. Our research provides strong evidence for the discriminatory nature of workplace segregation faced by Black Americans within the federal government.

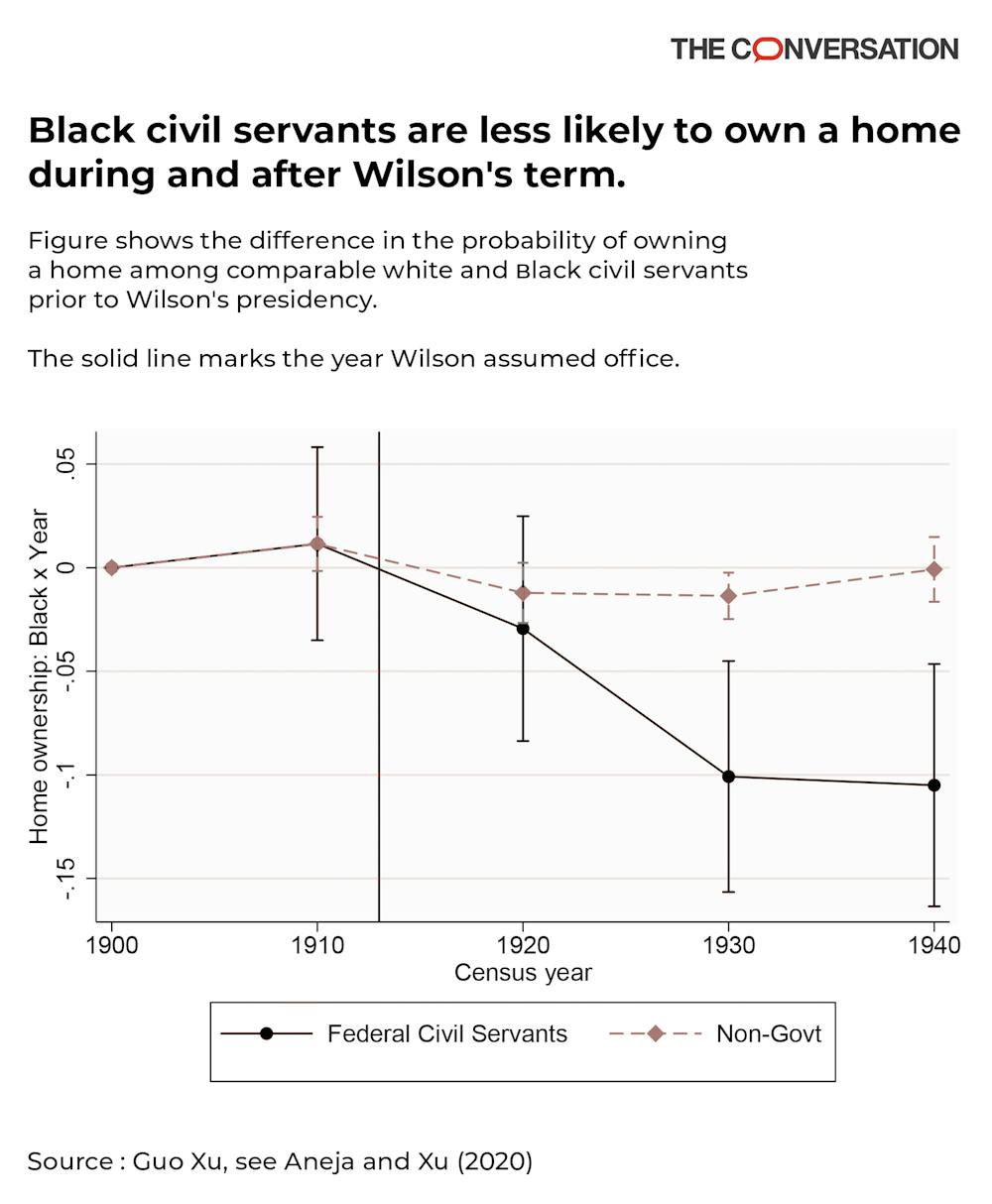

Black workers targeted by federal policies earned less money and had less capacity to own a home.Figure by Aneja and Xu (2020)

Our research shows that the damage caused by working under discriminatory conditions persisted well beyond Wilson’s presidency. The same Black civil servants victimized by discrimination in federal employment were also less likely to own a home in 1920, 1930 and 1940, almost three decades after Wilson was elected. Moreover, the school-age children of Black civil servants who served in the Wilson administration went on to have poorer-quality lives than their young white counterparts in terms of their overall earnings and quality of employment in adulthood.

This research can help to contribute to the understanding of the roots of economic disparities. A policy of racial discrimination – even if implemented temporarily – has lasting negative effects. A clearer understanding of historical discrimination can help to inform the design of policies aimed at remedying the painfully persistent racial inequities we observe today.

Republished with permission under license from The Conversation.

Until the 21st century, the contributions of African-American soldiers in World War II barely registered in America’s collective memory of that war.

The “tan soldiers,” as the black press affectionately called them, were also for the most part left out of the triumphant narrative of America’s “Greatest Generation.” In order to tell their story of helping defeat Nazi Germany in my 2010 book, “Breath of Freedom,” I had to conduct research in more than 40 different archives in the U.S. and Germany.

Two U.S. soldiers on Easter morning, 1945. NARA

When a German TV production company, together with Smithsonian TV, turned that book into a documentary, the filmmakers searched U.S. media and military archives for two years for footage of black GIs in the final push into Germany and during the occupation of post-war Germany.

They watched hundreds of hours of film and discovered less than 10 minutes of footage. This despite the fact that among the 16 million U.S. soldiers who fought in World War II, there were about one million African-American soldiers.

They fought in the Pacific, and they were part of the victorious army that liberated Europe from Nazi rule. Black soldiers were also part of the U.S. Army of occupation in Germany after the war. Still serving in strictly segregated units, they were sent to democratize the Germans and expunge all forms of racism.

A soldier paints over a swastika.NARA

It was that experience that convinced many of these veterans to continue their struggle for equality when they returned home to the U.S. They were to become the foot soldiers of the civil rights movement – a movement that changed the face of our nation and inspired millions of repressed people across the globe.

As a scholar of German history and of the more than 70-year U.S. military presence in Germany, I have marveled at the men and women of that generation. They were willing to fight for democracy abroad, while being denied democratic rights at home in the U.S. Because of their belief in America’s “democratic promise” and their sacrifices on behalf of those ideals, I was born into a free and democratic West Germany, just 10 years after that horrific war.

Fighting racism at home and abroad

By deploying troops abroad as warriors for and emissaries of American democracy, the military literally exported the African-American freedom struggle.

Beginning in 1933, when Adolf Hitler came to power, African-American activists and the black press used white America’s condemnation of Nazi racism to expose and indict the abuses of Jim Crow at home. America’s entry into the war and the struggle against Nazi Germany allowed civil rights activists to significantly step up their rhetoric.

Langston Hughes’ 1943 poem, “From Beaumont to Detroit,” addressed to America, eloquently expressed that sentiment:

“You jim crowed me / Before hitler rose to power- / And you are still jim crowing me- / Right now this very hour.”

Believing that fighting for American democracy abroad would finally grant African-Americans full citizenship at home, civil rights activists put pressure on the U.S. government to allow African-American soldiers to “fight like men,” side by side with white troops.

The military brass, disproportionately dominated by white Southern officers, refused. They argued that such a step would undermine military efficiency and negatively impact the morale of white soldiers. In an integrated military, black officers or NCOs might also end up commanding white troops. Such a challenge to the Jim Crow racial order based on white supremacy was seen as unacceptable.

The manpower of black soldiers was needed in order to win the war, but the military brass got its way; America’s Jim Crow order was to be upheld. African-Americans were allowed to train as pilots in the segregated Tuskeegee Airmen. The 92nd Buffalo Soldiers and 93rd Blue Helmets all-black divisions were activated and sent abroad under the command of white officers.

Despite these concessions, 90 percent of black troops were forced to serve in labor and supply units, rather than the more prestigious combat units. Except for a few short weeks during the Battle of the Bulge in the winter of 1944 when commanders were desperate for manpower, all U.S. soldiers served in strictly segregated units. Even the blood banks were segregated.

‘A Breath of Freedom’

After the defeat of the Nazi regime, an Army manual instructed U.S. occupation soldiers that America was the “living denial of Hitler’s absurd theories of a superior race,” and that it was up to them to teach the Germans “that the whole concept of superiority and intolerance of others is evil.” There was an obvious, deep gulf between this soaring rhetoric of democracy and racial harmony, and the stark reality of the Jim Crow army of occupation. It was also not lost on the black soldiers.

Women’s Army Corps in Nuremberg, Germany, 1949.Library of Congress

Post-Nazi Germany was hardly a country free of racism. But for the black soldiers, it was their first experience of a society without a formal Jim Crow color line. Their uniform identified them as victorious warriors and as Americans, rather than “Negroes.”

Serving in labor and supply units, they had access to all the goods and provisions starving Germans living in the ruins of their country yearned for. African-American cultural expressions such as jazz, defamed and banned by the Nazis, were another reason so many Germans were drawn to their black liberators. White America was stunned to see how much black GIs enjoyed their time abroad, and how much they dreaded their return home to the U.S.

By 1947, when the Cold War was heating up, the reality of the segregated Jim Crow Army in Germany was becoming a major embarrassment for the U.S. government. The Soviet Union and East German communist propaganda relentlessly attacked the U.S. and challenged its claim to be the leader of the “free world.” Again and again, they would point to the segregated military in West Germany, and to Jim Crow segregation in the U.S. to make their case.

Coming ‘home’

Newly returned veterans, civil rights advocates and the black press took advantage of that Cold War constellation. They evoked America’s mission of democracy in Germany to push for change at home. Responding to that pressure, the first institution of the U.S. to integrate was the U.S. military, made possible by Truman’s 1948 Executive Order 9981. That monumental step, in turn, paved the way for the 1954 Supreme Court decision in Brown v. Board of Education.

Hosea Williams, World War II Army veteran and civil rights activist, rallies demonstrators in Selma, Ala. 1965.AP Photo

The veterans who had been abroad electrified and energized the larger struggle to make America live up to its promise of democracy and justice. They joined the NAACP in record numbers and founded new chapters of that organization in the South, despite a wave of violence against returning veterans. The veterans of World War II and the Korean War became the foot soldiers of the civil rights movement in the 1950s and 1960s. Medgar Evers, Amzie Moore, Hosea Williams and Aaron Henry are some of the better-known names, but countless others helped advance the struggle.

About one-third of the leaders in the civil rights movement were veterans of World War II.

They fought for a better America in the streets of the South, at their workplaces in the North, as leaders in the NAACP, as plaintiffs before the Supreme Court and also within the U.S. military to make it a more inclusive institution. They were also the men of the hour at the 1963 March on Washington, when their military training and expertise was crucial to ensure that the day would not be marred by agitators opposed to civil rights.

“We structured the March on Washington like an army formation,” recalled veteran Joe Hairston.

For these veterans, the 2009 and 2013 inaugurations of President Barack Obama were triumphant moments in their long struggle for a better America and a more just world. Many never thought they would live to see the day that an African-American would lead their country.

In ancient Athens, only the very wealthiest people paid direct taxes, and these went to fund the city-state’s most important national expenses – the navy and honors for the gods. While today it might sound astonishing, most of these top taxpayers not only paid happily, but boasted about how much they paid.

Money was just as important to the ancient Athenians as it is to most people today, so what accounts for this enthusiastic reaction to a large tax bill? The Athenian financial elite felt this way because they earned an invaluable payback: public respect from the other citizens of their democracy.

Athens in the fifth and fourth centuries B.C. had a population of free and enslaved people topping 300,000 individuals. The economy mostly focused on international trade, and Athens needed to spend large sums of money to keep things humming – from supporting national defense to the countless public fountains constantly pouring out drinking water all over the city.

Much of this income came from publicly owned farmland and silver mines that were leased to the highest bidders, but Athens also taxed imports and exports and collected fees from immigrants and prostitutes as well as fines imposed on losers in many court cases. In general, there were no direct taxes on income or wealth.

As Athens grew into an international power, it developed a large and expensive navy of several hundred state-of-the-art wooden warships called triremes – literally meaning three-rowers. Triremes cost huge amounts of money to build, equip and crew, and the Athenian financial elites were the ones that paid to make it happen.

Triremes were the most advanced and expensive military technology of the ancient Mediterranean, and rich Athenians funded them out of their own pockets.Marsyas via Wikimedia Commons, CC BY

The top 1% of male property owners supported the saving or salvation of Athens –called “soteria” – by performing a special kind of public service called “leitourgia,” or liturgy. They served as a trireme commander, or “trierarch,” who personally funded the operating costs of a trireme for an entire year and even led the crew on missions. This public service was not cheap. To fund their liturgy as a trierarch, a rich taxpayer spent what a skilled worker earned in 10 to 20 years of steady pay, but instead of dodging this responsibility, most embraced it.

Running warships was not the only responsibility the rich had to national defense. When Athens was at war – which was most of the time – the wealthy had to pay contributions in cash called “eisphorai” to finance the citizen militia. These contributions were based on the value of their property, not their income, which made them in a sense a direct tax on wealth.

To the ancient Athenians, physical military might was only part of the equation. They also believed that the salvation of the state from outside threats depended on a less tangible but equally crucial and costly source of defense: the favor of the gods.

To keep these powerful but fickle divine protectors on their side, the Athenians built elaborate temples, performed large sacrifices and organized lively public religious festivals. These massive spectacles featured musical extravaganzas and theater performances that were attended by tens of thousands of people and were hugely expensive to throw.

Just as with trieremes, the richest Athenians paid for these festivals by fulfilling festival liturgies. Serving as a chorus leader, for example, meant paying for the training, costumes and living expenses for large groups of performers for months at a time.

None of the financial elite of ancient Athens prided themselves on scamming the Athenian equivalent of the IRS. Just the opposite was true: They paid, and even boasted in public – truthfully – that they often had paid more than required when serving as a trierarch or chorus leader.

Of course, not every member of the superrich at Athens behaved like a patriotic champion. Some Athenian shirkers tried to escape their liturgies by claiming other people with more property ought to shoulder the cost instead of themselves, but this attempted weaseling out of public service never became the norm.

This social capital was so valuable because Athenian culture held civic duty in high regard. If a rich Athenian hoarded his wealth, he was mocked and labeled a “greedy man” who “borrows from guests staying his house” and “when he sells wine to a friend, he sells it watered!”

The Choragic Monument of Lysicrates was erected in 335 B.C. by the liturgist Lysicrates after his play won first prize, and it still stands today.C messier via Wikimedia Commons, CC BY-SA

Social wealth, not monetary riches

The social rewards that tax payments earned the rich had long lives. A liturgist who financed the chorus of a prize-winning drama could build himself a spectacular monument in a conspicuous downtown location to announce his excellence to all comers for all time.

So, too, the Athenians infused that designation with immense power. To be a rich taxpayer who was good and useful to his fellow citizens counted even more than money in the bank. And this invaluable public service profited all Athenians by keeping their democracy alive century after century.

Republished with permission under license from The Conversation.

Court.rchp.com Editorial Note: Missouri is one of only four states that do not provide any state wide mail in ballot tracking, however, in the St. Louis area, tracking is available.

St. Louis City:Go to STLCityBallotTracking.com, Enter the “Ballot Track ID” from your ballot stub. You may also scan the square QR code on the stub and the code will take you right to the results. Once the St. Louis Board of Election Commissioners has received your ballot, they’ll let you know by updating your ballot tracking page with a third green checkmark.

St. Charles County: There are a few steps to tracking your ballot in St. Charles County. First, visit sccmo.org/410/Election-Authority and then scroll down just a little to the “Nov. 3, 2020 General Election Information” list. Then click the second option which is “Track your Absentee by Mail ballot.” Then enter your information in their tracking system and you should be able to track your ballot from there.

Jefferson County: There is no tracking website, but if you call the County Clerk’s office and give them your name and address, they’ll look you up and confirm that your ballot has been received. Their phone number is 636-797-5486 and once you get the voice recording press “2” on your phone for the Voter Registration and Elections Department.

by Steven Mulroy, University of Memphis

Many voters who want to participate in the election by mail are concerned about when they’ll receive their ballot – and whether it will get back in time to be counted.

At the same time, recent changes at the U.S. Postal Service have caused slowdowns in mail delivery. The Postal Service itself has warned states that ballots mailed by election officials close to Election Day may not reach voters in time. A federal court has issued a nationwide order giving election-related mail priority in Postal Service processing.

Nevertheless, anecdotal reports abound of voters who applied for absentee ballots and are still waiting for them weeks later.

And on Oct. 19, the U.S. Supreme Court accommodated potential mail delays by ruling that Pennsylvania may count ballots that arrive through the end of Friday, Nov. 6 – three days after Election Day.

Different states have different rules about who can cast their ballots by mail; I was involved in a nonpartisan lawsuit that expanded access to voting by mail in Tennessee.

Fortunately, almost everyone who is allowed to vote by mail can stay on top of where those ballots are. In 44 states and the District of Columbia, a unified system allows all voters to see when their request for a ballot by mail was received, when the ballot was mailed to them and when the completed ballot was received back at the local election office.

Two other states provide online tracking for members of the military and civilian citizens who live overseas – groups that have special mail ballot protections under federal law. In the remaining four states without a statewide ballot-tracking system, some counties and municipalities may have their own online versions – or may be able to update voters who contact the office by phone or in person.

The Postal Service, election officials and other experts recommend that people conservatively allow a week for the ballot to arrive at their home from the election office, and a week for it to get back so it can be counted. It may take less time, and in some places you can speed things up by using an official drop box to return your ballot without relying on the mail.

In either case, you can keep an eye on your ballot to make sure it has arrived and been accepted for counting. And if it hasn’t arrived yet, or has been rejected for some reason, you’ll know to contact local election officials to see what to do so your vote can count.

Republished with permission under license from The Conversation.

As a political battle over the Supreme Court’s direction rages in Washington with President Donald Trump’s nomination of Amy Coney Barrett, history shows that political contests over the ideological slant of the Court are nothing new.

In the 1860s, President Abraham Lincoln worked with fellow Republicans to shape the Court to carry out his party’s anti-slavery and pro-Union agenda. It was an age in which the court was unabashedly a “partisan creature,” in historian Rachel Shelden’s words.

Justice John Catron had advised Democrat James K. Polk’s 1844 presidential campaign, and Justice John McLean was a serial presidential contender in a black robe. And in the 1860s, Republican leaders would change the number of justices and the political balance of the Court to ensure their party’s dominance of its direction.

Overhauling the Court

When Lincoln became president in 1861, seven Southern states had already seceded from the Union, yet half of the Supreme Court justices were Southerners, including Chief Justice Roger B. Taney of Maryland. One other Southern member had died in 1860, without replacement. All were Democratic appointees.

The Court was “the last stronghold of Southern power,” according to one Northern editor. Five sitting justices were among the court’s 7-2 majority in the racist 1857 Dred Scott v. Sandford ruling, in which Taney wrote that Black people were “so far inferior that they had no rights which the white man was bound to respect, and that the negro might justly and lawfully be reduced to slavery for his benefit.”

Some Republicans declared it “the duty of the Republican Party to reorganize the Federal Court and reverse that decision, which … disgraces the judicial department of the Federal Government.”

After Lincoln called in April, 1861 for 75,000 volunteers to put down the Southern rebellion, four more states seceded. So did Justice John Archibald Campbell of Georgia, who resigned on April 30.

Chief Justice Taney helped the Confederacy when he tried to restrain the president’s power. In May 1861, he issued a writ of habeas corpus in Ex Parte Merryman declaring that the president couldn’t arbitrarily detain citizens suspected of aiding the Confederacy. Lincoln ignored the ruling.

To counter the court’s southern bloc, Republican leaders used judicial appointments to protect the president’s power to fight the Civil War. The Lincoln administration was also looking ahead to Reconstruction and a governing Republican majority.

Nine months into his term, Lincoln declared that “the country generally has outgrown our present judicial system,” which since 1837 had comprised nine federal court jurisdictions, or “circuits.” Supreme Court justices rode the circuit, presiding over those federal courts.

Republicans passed the Judiciary Act of 1862, overhauling the federal court system by collapsing federal circuits in the South from five to three while expanding circuits in the North from four to six. The old ninth circuit, for example, included just Arkansas and Mississippi. The new ninth included Missouri, Kansas, Iowa and Minnesota instead. Arkansas became part of the sixth, and Mississippi, the fifth.

In 1862, after Campbell’s resignation and McLean’s death, Lincoln filled three open Supreme Court seats with loyal Republicans Noah H. Swayne of Ohio, Samuel Freeman Miller of Iowa and David Davis of Illinois. The high court now had three Republicans and three Southerners.

The 1863 Prize cases tested whether Republicans had managed to secure a friendly court. At issue was whether the Union could seize American ships sailing into blockaded Confederate ports. In a 5-4 ruling, the high court – including all three Lincoln appointees – said yes.

Congressional Republicans spied a way to expand the court while solving what amounted to a geopolitical judicial problem. In 1863, Congress created a new tenth circuit by adding Oregon, which had become a state in 1859, to California’s circuit. The Tenth Circuit Act also added a tenth Supreme Court justice. Lincoln elevated pro-Union Democrat Stephen Field to that seat.

After Lincoln’s assassination in April 1865, President Andrew Johnson of Tennessee, who succeeded him, soon began undoing Lincoln’s achievements. He was a Unionist Democrat given the vice presidency as an olive branch to the South. He rewarded that gesture in part by pardoning rank and file Confederates. Johnson also opposed civil rights for newly-freed African Americans.

He also threatened to appoint like-minded judges. But the Republican-dominated Congress blocked Johnson from elevating unreconstructed Rebels to the high court. The Judicial Circuits Act of 1866 shrank the number of federal circuits to seven and held that no Supreme Court vacancies would be filled until just seven justices remained.

The Philadelphia Evening Telegraph’s Democratic editor sighed that at least Republicans “cannot pack the Supreme Court at this moment.”

Republicans refused to consider nominating Johnson in 1868, picking General Ulysses S. Grant instead. He won, and after President Grant’s inauguration, Congress passed the Circuit Judges Act of 1869, raising back to nine the number of Supreme Court justices.

Shortly after, Republicans faced a financial problem of their own making.

Beginning in 1862, Congress had passed three Legal Tender Acts – initially to help finance the war, authorizing debt payments using paper money not backed by gold or silver. Then-Treasury Secretary and current Chief Justice Salmon P. Chase had crafted the legislation.

But in an 1870 case, Hepburn v. Griswold, Chase reversed himself in a 4-3 decision, ruling the Legal Tender Acts unconstitutional. That threatened national monetary policy and Republicans’ cozy relationship with industries reliant on government sponsorship.

President Grant, preparing for Chase’s ruling, was already working on a political solution. On the day of the Hepburn decision, he appointed two pro-paper-money Supreme Court nominees, William Strong of Pennsylvania and Joseph P. Bradley of New York. Comparing the Republican administration to “a brokerage office,” a Democratic newspaper howled that “the attempt to pack the supreme court to secure a desired judicial decision … (has) brought shame and humiliation to an entire people.”

It also brought a Republican majority to the high court for the first time.

Chief Justice Chase opposed revisiting the paper money issue. But the Supreme Court about-faced, ruling 5-4 in the 1871 cases Knox v. Lee and Parker v. Davis that the government could indeed print paper money to pay debts. Chase died in 1873, and his successor Morrison Waite championed the Republican pro-business agenda.

Careful what you wish for

Republican transformation of the federal judiciary in the 1860s and 1870s served the party well in the Civil War and constructed a legal framework for a modernizing industrial economy.

But in the end Lincoln and Grant’s high court appointments ended up being disastrous for civil rights. Justices Bradley, Miller, Strong and Waite tended to constrain civil rights protections like the Fourteenth Amendment, which guarantees equal protection of laws. Their rulings in United States v. Cruikshank in 1876 and Civil Rights Cases in 1883 both sounded the retreat on Black civil rights.

In remaking the court in Republicans’ image, the party got what it wanted – but not what was needed to fulfill the promise of “a new birth of freedom.”

Republished with permission under license from The Conversation.

After a pause for the pandemic, debt buyers are back in the courts, suing debtors by the thousands.

by Paul Kiel and Jeff Ernsthausen,

Earlier this year, the pandemic swept across the country, killing 100,000 Americans by the spring, shuttering businesses and schools, and forcing people into their homes. It was a great time to be a debt collector.

In August, Encore Capital, the largest debt buyer in the country, announced that it had doubled its previous record for earnings in a quarter. It primarily had the CARES Act to thank: The bill delivered hundreds of billions of dollars worth of stimulus checks and bulked-up unemployment benefits to Americans, while easing pressures on them by halting foreclosures, evictions and student loan payments. There was no ban on collections of old credit card bills, Encore’s specialty.

At the same time, the pandemic compelled households to cut spending. Finding themselves with enough money to settle old debts, people responded to collectors’ calls and letters. Debt-buying executives couldn’t help marveling at their good fortune. All this created “a perfect storm from a cash perspective,” the CEO of Portfolio Recovery Associates, Encore’s main competitor, told Wall Street analysts.

After its record second quarter, analysts expect Encore to blow past $200 million in profit this year and reward stockholders with 40% earnings growth compared with last year. Portfolio Recovery is set for similar growth. The share prices of both have soared off their early April lows.

Investors didn’t even show much concern when, in early September, the Consumer Financial Protection Bureau sued Encore, saying that it had broken the terms of a consent agreement struck in 2015. The agency had previously charged the company with “pressuring consumers with false statements and churning out lawsuits using robo-signed court documents,” as it said at the time. (In a statement, Encore said the CFPB’s recent suit was unnecessary because it had fixed the alleged problems “years ago.”)

In recent months, the only real bad news for debt buyers was that local courts across the country temporarily shut down. Debt collection lawsuits provide a key source of revenue for the companies, a way to extract payment from consumers, typically low-income, who don’t offer it up.

But now even that hiccup is over. After a bit of a lull in the spring, Encore and other debt buyers are back at it, filing suits by the thousands every week, according to ProPublica’s analysis of state court filings.

In August alone, Encore filed about 1,000 suits in Indiana and over 2,000 suits in the metro Atlanta area. Other debt buyers jumped back in as well. In Chicago, Portfolio Recovery filed over 3,000 suits in July, while LVNV, a major debt buyer privately owned by Sherman Financial Group, filed over 2,700 suits in Maryland in August. For all these companies, ProPublica found, the volume was well above the number they’d filed before the coronavirus arrived, in January or February of this year. No national numbers on suits exist.

In statements, the companies said they have been actively working with consumers during the COVID-19 pandemic and only sue as a last resort on a small portion of accounts.

Elizabeth A. Kersey, a spokesperson for Portfolio Recovery, said the company’s hardship program “allows for the suspension of collection efforts for ninety (90) days upon notification of a hardship event.” The company is currently not seeking new orders to seize debtors’ wages or bank account funds, she said.

Ryan Bell, an Encore executive, said, “We have consistently and proactively communicated to consumers the various relief options we’ve put in place in response to COVID-19, including temporarily stopping collections.” The company said it had stopped seeking orders to garnish bank accounts. It is, however, seizing wages.

Sherman Financial did not respond to requests for comment.

If Congress is unable to pass any further stimulus , unemployment is likely to remain high. In that scenario, debt buying companies and the banks that sell defaulted accounts to them expect more Americans to fall behind on their credit card bills over the coming months.

Even that scenario turns out to be rosy for the debt buyers. While good times can mean that Encore collects on more debt than it expected, bad times typically bring a glut of people suffering under loans they cannot repay. The result is that Encore can scoop up the raw materials for its profit machine — defaulted accounts — more cheaply. Or as Encore CEO Ashish Masih put it to Wall Street: The company is “particularly excited about the prospects for increased supply in the future.”

“The same giant debt buyers known for fighting consumer protection laws at every turn have been raking in cash during this pandemic,” Sen. Elizabeth Warren, D-Mass, told ProPublica. “They are now licking their chops in anticipation of profiting even more off families who have their hours further cut or can’t find a job, and can’t keep up with their bills or their mortgage. This is disgraceful and reinforces the need for Congress to protect consumers and small businesses from this predatory behavior.”

In recent years, Encore has bought around 2 million to 3 million U.S. accounts per year, according to public filings. Last year, on average, the company paid 8.6 cents on the dollar for each account. For a typical debt of $3,142, Encore paid $271.

To earn a profit on that investment, Encore and other debt buyers pursue debtors in near perpetuity. Encore is still collecting tens of millions of dollars each year from debts it bought in 2009 or earlier. The key to that persistence is the courts.

Since the early 2000s, debt buyers have flooded local courts nationwide with suits. The companies regularly account for more than a quarter of all debt collection cases in a given jurisdiction, according to ProPublica’s review of collection filings over several states.

ProPublica did find one exception among the major banks that commonly file a significant number of suits: Citigroup, which resumed filing suits at its normal levels in July. The bank, for instance, filed over 200 suits in Oklahoma in August, more than it had filed there in January and February combined.

In a statement, Citi spokesperson Jennifer Bombardier said the bank has a special assistance program for customers impacted by COVID-19 and that it is not seeking to garnish the bank accounts of customers it has sued. The bank also did not sell charged-off accounts to debt buyers “for up to 120 days” in the states “most impacted by COVID-19,” she said.

Encore sued Nicole Campbell of Brooklyn, New York, in July. Her first task was to figure out what to do. The suit was over $3,023.76 in debt she incurred years ago with CareCredit, a card offered by Synchrony Bank to people who need to cover medical costs, such as dentistry and eyecare. She knew she should answer the complaint by going to the courthouse, but she was wary of going there during the pandemic and wasn’t even sure whether it was open.

Even attorneys have difficulty finding their way. “Courts have been returning to full operation, but there’s so much confusion as to what’s happening,” said Susan Shin, legal director of the New Economy Project in New York City. “It’s hard to know what to advise people on what to do with their case.”

With help from an attorney with the New Economy Project, Campbell responded to the suit by mail. She’s not sure what to expect next but said she doesn’t have much time to worry about it. She cares for three boys, 5, 11 and 14, on her own and has to figure out how to get them to school on the city’s part-time schedule while helping them with online lessons when they’re home. She juggles this with her own job as a customer service rep: That also has a rotating, part-time schedule in order to minimize the number of people in the office.

“It’s crazy to me they’re filing all this during this time when there’s so much going on,” she said.

Such collection suits are most common among workers with income under $40,000 per year and particularly common in mostly Black neighborhoods. The suits routinely result in judgments, which in turn usually result in attempts at garnishment, according to a ProPublica analysis of Missouri court filings. Past studies have put the number of workers who have their wages garnished each year at around 4 million. In most states, plaintiffs can seize up to a quarter of a worker’s take-home pay or clean out their bank account.

In recent years, when state legislatures have moved to protect more funds from garnishment, Encore has been there to oppose the measures. In 2018, a Connecticut bill proposed to automatically protect up to $1,000 in a bank account. An Encore executive, Sonia Gibson, argued against it, writing in a letter, “Since the average amount we collect through bank garnishments is typically around $700, an automatic exemption of $1,000 would leave us unable to use bank garnishments.” The bill died.

Last year in California, Encore joined with other debt buyers to combat a similar bill that aimed to protect around $1,700.

“It was a really huge fight,” said Ted Mermin, head of the California Low-Income Consumer Coalition and a professor at the University of California, Berkeley, School of Law. “And you’ve got to think, ‘Why?’ Who on earth thinks it’s a good idea to take someone’s last dollar? The only people who would do this are debt collectors who have no ongoing relationship with someone.” The bill narrowly passed and became law.

In Washington state, lawmakers last year sought to protect more workers from wage garnishment. Under federal law, earnings above $217.50 in a week are eligible to be seized, a level that has remained the same since 2009 because it’s tied to the $7.25 federal minimum wage. The Washington bill, which ultimately passed, aimed to tie the exemption to the state’s much higher minimum wage, which this year is $13.50 an hour. In 2020, about $472.50 in weekly take-home pay would be protected. That was much too high for Encore. Gibson argued in a letter that people earning that much shouldn’t be “completely exempt from garnishment.”

As an alternative to automatic protections, Encore generally argues that consumers should have to file exemptions in court to demonstrate they really can’t afford to have their money taken. Consumer advocates say that such exemptions, which often exist in state laws, are rarely invoked by debtors because they either don’t know about them or don’t understand the process.

On paper, Randall Ward would seem to be well-insulated from garnishment. He lives in the small town of Marianna, Florida, and state law protects the wages of anyone deemed the “head of household,” which is defined as someone who earns more than half the household’s income and has dependents. Since Ward helps care for his 20-year-old son with Down syndrome and a granddaughter, his pay from his job as a manager at a Waffle House is eligible for protection.

But when Encore, after having won a judgment against Ward the previous year, sought to garnish his wages this past February, Ward didn’t understand that he qualified for the “head of household” exemption. So, starting in March, Encore began taking a quarter of Ward’s take-home pay. The size of the debt, a Citibank card that had ballooned to $5,220 with interest and court costs, meant that Ward, even with what he’s proud to call a “good job,” was in for many lean months.

The only way to make ends meet, he said, was to cancel health insurance for himself, his son and his wife, “because I could not pay the bills if I didn’t do it.”

Then the virus forced his restaurant to close for several weeks and his pay stopped altogether. The family was without income as he waited for his unemployment claim to go through. When, finally, he could go back to work, the garnishments returned. Encore has said in public statements that it looks to work with consumers, especially those who’ve been impacted by COVID-19. Ward said that was not his experience.

“They’re just ruthless about it,” he said. “I would hate to see that happen to anybody.”

Encore declined to comment on individual accounts.

Collection suits can have a lasting negative effect on consumers. A recent study by economists from Dartmouth’s Tuck School of Business and the University of California, San Diego, focused on debtors who, after being sued, agreed to pay in order to avoid garnishment. The settlements left consumers worse off: They were more likely to fall behind on other debts or end up in foreclosure or bankruptcy, the study found. The main reason was that paying up on one debt had drained those consumers’ cash buffer and that left them vulnerable to falling behind on others.

Even in good economic times, low-income consumers live on the edge, so the CARES Act aid was particularly helpful to them. According to a Federal Reserve survey, the temporary $600 boost to weekly unemployment insurance benefits actually resulted in higher pay for about 40% of those who received them. On top of that came the $1,200 stimulus checks ($2,400 for married couples) with an additional $500 for each child.

In July, the Fed found households with income under $40,000 a year had significantly more savings than normal: Whereas last year just 39% said they would have covered an unexpected $400 expense with cash, this summer, 48% said they would.

Debt collectors were a clear beneficiary of those extra funds. According to a survey by the Bureau of Labor Statistics, while most people used the stimulus payments to buy food and other essentials, about 25% used at least some of the money to pay down debts.

But Felipe Severino, a Tuck School of Business professor and one of the authors of the paper on debt collection settlements, said there may be negative long-term consequences for households who used the extra money to settle older debts. The companies say they do not charge interest on the old, charged-off debts they collect so the debts are not growing.

“I would argue it’s not a very good use of their money,” he said. With less of a safety net, those households are more likely to find themselves behind on their bills again.

Furthermore, he said, stimulative government aid like the CARES Act is meant to be “spent and magnify across the economy” in the near term by, for instance, leading to increased purchases at local businesses. That doesn’t happen when the money goes to debt collectors.

The flood of government aid, along with the sudden contraction in spending due to COVID-19, has led to an unpredictable economy, one where unemployment has shot up without the usual tide of delinquencies, bankruptcies and foreclosures. But now, banks are predicting that tide to finally arrive in the coming months.

In July, Capital One reported a loss for the quarter despite delinquencies actually going down. The reason was the bank set aside $2.9 billion as a provision for future credit losses, a kind of safety net for the future.

Encore did not appear to need such precautions. “Our liquidity puts us in a strong position to capture the substantial purchasing opportunity, which we believe is sure to follow,” Masih, the CEO, told analysts.

Republished with permission under license from ProPublica.

Lawsuit trends highlight need to modernize civil legal systems

Overview

The business of state civil courts has changed over the past three decades. In 1990, a typical civil court docket featured cases with two opposing sides, each with an attorney, most frequently regarding commercial matters and disputes over contracts, injuries, and other harms. The lawyers presented their cases, and the judge, acting as the neutral arbiter, rendered a decision based on those legal and factual arguments.

Thirty years later, that docket is dominated not by cases involving adversaries seeking redress for an injury or business dispute, but rather by cases in which a company represented by an attorney sues an individual, usually without the benefit of legal counsel, for money owed. The most common type of such business-to-consumer lawsuits is debt claims, also called consumer debt and debt collection lawsuits. In the typical debt claim case, a business—often a company that buys delinquent debt from the original creditor—sues an individual to collect on a debt. The amount of these claims is almost always less than $10,000 and frequently under $5,000, and typically involves unpaid medical bills, credit card balances, auto loans, student debt, and other types of consumer credit, excluding housing (mortgage or rent).

For more than a decade, the American Bar Association and legal advocacy organizations such as the Legal Services Corporation and the National Legal Aid and Defenders Association have sounded alarms about worrisome trends underway in the civil legal system. And court leaders have taken notice. In 2016, a committee of the Conference of Chief Justices, a national organization of state supreme court heads, issued a report recommending that courts enact rules to provide a more fair and just civil legal system, especially with respect to debt collection cases. Chief justices of various supreme courts, with support from private foundations, have established task forces to probe the issue further.

However, until relatively recently, these discussions were largely confined to court officials, legal aid advocates, and other stakeholders concerned about the future of the legal profession. In most states, policymakers have not been a part of conversations about how and why civil court systems are shifting; the extent to which the changes might lead to financial harm among American consumers, especially the tens of millions of people in the U.S. who are stuck in long-term cycles of debt; and potential strategies to address these issues.

To help state leaders respond to the changing realities in civil courts, The Pew Charitable Trusts sought to determine what local, state, and national data exist on debt collection cases and what insights those data could provide. The researchers supplemented that analysis with a review of debt claims research and interviews with consumer experts, creditors, lenders, attorneys, and court officials.

The key findings are:

Fewer people are using the courts for civil cases. Civil caseloads dropped more than 18 percent from 2009 to 2017. Although no research to date has identified the factors that led to this decline, previous Pew research shows lack of civil legal problems is not one of them: In 2018 alone, more than half of all U.S. households experienced one or more legal issues that could have gone to court, including 1 in 8 with a legal problem related to debt.

Debt claims grew to dominate state civil court dockets in recent decades. From 1993 to 2013, the number of debt collection suits more than doubled nationwide, from less than 1.7 million to about 4 million, and consumed a growing share of civil dockets, rising from an estimated 1 in 9 civil cases to 1 in 4. In a handful of states, the available data extend to 2018, and those figures suggest that the growth of debt collections as a share of civil dockets has continued to outpace most other categories of cases. Debt claims were the most common type of civil case in nine of the 12 states for which at least some court data were available—Alaska, Arkansas, Colorado, Missouri, Nevada, New Mexico, Texas, Utah, and Virginia. In Texas, the only state for which comprehensive statewide data are available, debt claims more than doubled from 2014 to 2018, accounting for 30 percent of the state’s civil caseload by the end of that five-year period.

People sued for debts rarely have legal representation, but those who do tend to have better outcomes. Research on debt collection lawsuits from 2010 to 2019 has shown that less than 10 percent of defendants have counsel, compared with nearly all plaintiffs. According to studies in multiple jurisdictions, consumers with legal representation in a debt claim are more likely to win their case outright or reach a mutually agreed settlement with the plaintiff.

Debt lawsuits frequently end in default judgment, indicating that many people do not respond when sued for a debt. Over the past decade in the jurisdictions for which data are available, courts have resolved more than 70 percent of debt collection lawsuits with default judgments for the plaintiff. Unlike most court rulings, these judgments are issued, as the name indicates, by default and without consideration of the facts of the complaint—and instead are issued in cases where the defendant does not show up to court or respond to the suit. The prevalence of these judgments indicates that millions of consumers do not participate in debt claims against them.

Default judgments exact heavy tolls on consumers. Courts routinely order consumers to pay accrued interest as well as court fees, which together can exceed the original amount owed. Other harmful consequences can include garnishment of wages or bank accounts, seizure of personal property, and even incarceration.

States collect and report little data regarding their civil legal systems, including debt cases. Although 49 states and the District of Columbia provide public reports of their cases each year, 38 and the district include no detail about the number of debt cases. And in 2018, only two states provided figures on default judgments in any of their state’s debt cases. Texas is the only state that reports on all types of cases, including outcomes, across all courts.

States are beginning to recognize and enact reforms to address the challenges of debt claims. From 2009 to 2019, 12 states made changes to policy—seven via legislation and five through court rules—to improve courts’ ability to meet the needs of all debt claim litigants. Examples of such reforms include ensuring that all parties are notified about lawsuits; requiring plaintiffs to demonstrate that the named defendant owes the debt sought and that the debt is owned by the plaintiff; and in some states, enhanced enforcement of the prohibitions on lawsuits for which the legal right to sue has expired.

Based on the findings of this analysis and these promising efforts in a handful of states, Pew has identified three initial steps states can take to improve the handling of debt collection cases:

Track data about debt claims to better understand the extent to which these lawsuits affect parties and at which stages of civil proceedings courts can more appropriately support litigants.

Review state policies, court rules, and common practices to identify procedures that can ensure that both sides have an opportunity to effectively present their cases.

Modernize the relationship between courts and their users by providing relevant and timely procedural information to all parties and moving more processes online in ways that are accessible to users with or without attorneys.

In 2010, the Federal Trade Commission (FTC) issued a report on the lack of adequate service to consumers in state courts that concluded, “The system for resolving disputes about consumer debts is broken.”1 In the decade since, this problem has not abated and if anything has become more acute. Furthermore, the challenges that this report reviews regarding debt collection cases epitomize challenges facing the civil legal system nationwide. This report summarizes important but inadequately studied trends in civil litigation, highlights unanswered questions for future research, and outlines some initial steps that state and court leaders can take to ensure that civil courts can satisfy their mission to serve the public impartially.

Methods

This study involved a three-step approach to analyze debt collection lawsuit trends in state courts and the significance for consumers. To identify common characteristics and potential consequences of these cases, Pew researchers conducted a literature review of approximately 70 peer-reviewed and gray studies and performed semistructured interviews with experts from state and local courts, consumer advocacy organizations, and the credit and debt collection industries. To analyze the volume of debt claims in the United States and the extent to which courts track and report relevant data, researchers reviewed data from the National Center for State Courts (NCSC), including national caseload statistics from 2003 to 2017 and breakdowns of civil case types in 1993 and 2013, the most recent year for which this level of detail is available. Researchers also collected and analyzed annual court statistical reports for all 50 states and the District of Columbia from 2017 and, where available, from 2005, 2009, 2013, and 2018. Pew researchers conducted quality control for each step to minimize errors and bias. For more information, see the full methodological appendix.

Fewer people are using the courts for civil cases

Beginning in at least the 1980s and continuing through the first decade of the 21st century, caseload volume in civil courts was on an upward trajectory.2 After peaking in 2009, however, it began to decline and by 2017 had dropped to levels not seen in 20 years.3 (See Figure 1.)

Court systems in 44 states, the District of Columbia, and Puerto Rico reported total civil caseloads to NCSC’s Court Statistics Project in 2009 and 2017, and of those, 41 systems described lower caseloads over that span, both in raw numbers and per capita.4

A full examination of drivers of the decline in civil caseloads is outside the scope of this analysis. However, evidence indicates that the drop is not the result of a decrease in legal issues that people could bring to the court. A recent Pew survey found that in 2018, more than half of U.S. households had a legal issue that could have been resolved in court, and that 1 in 4 households had two or more such issues.5;

Civil Courts and Available Data

State courts hear cases in five categories: criminal, civil, family, juvenile, and traffic. For the purposes of this report, and in keeping with the way courts typically divide their dockets, civil cases are organized into five categories:

Debt collection: Suits brought by original creditors or debt buyers claiming unpaid medical, credit card, auto, and other types of consumer debt exclusive of housing (e.g., mortgage or rent).

Mortgage foreclosure: Suits brought by banks and other mortgage lenders seeking possession of a property as collateral for unpaid home loans.

Landlord-tenant: Predominantly eviction proceedings, with a smaller subset of suits brought by landlords for unpaid rent.

Tort: Personal injury and property damage cases; medical malpractice; automobile accidents; negligence; and other claims of harm.

Other: Other contract disputes; real property; employment; appeals from administrative agencies; civil cases involving criminal proceedings;6 civil harassment petitions; and “unknown” cases where the case type was undefined or unclear.

Further, state civil courts are tiered based on the dollar amount of the claims they hear:7

General civil matters, characterized by high dollar amounts (minimum value of $12,000 to $50,000, depending on the state; no maximum).

Limited civil matters of moderate dollar amounts (minimum value of zero to $10,000 and maximum of $20,000 to $100,000, depending on the state).

Small claims with the lowest dollar amounts (no minimum value; maximum of $2,500 to $25,000, depending on the state).

State laws dictate the jurisdiction—city, county, state, etc.—in which a plaintiff can file a suit and, based on the dollar amount of the claim, the tier of court appropriate to the claim. Courts that disaggregate their data in annual statistical reports typically report on claims filed in the general and limited civil courts based on the above five case types (or some variation). However, most states do not disaggregate information on claims filed in small claims jurisdiction courts.

Most civil cases today are brought by businesses against individuals for money owed

The most recent national data available show that, as the overall volume of cases has declined, business-to-consumer suits, particularly debt collections, mortgage foreclosure, and landlord-tenant disputes, have come to account for more than half of civil dockets.8 (See Figure 2.) As a committee of the Conference of Chief Justices put it in 2016, “Debt collection plaintiffs are almost always corporate entities rather than individuals, and landlord-tenant plaintiffs are often so.”9

As of 2013, civil business-to-consumer lawsuits exceeded all court categories except traffic and criminal, and that same year, state courts heard more business-to-consumer cases than family (or “domestic relations”) and juvenile cases combined.10 (See Figure 3.)

Although organizing civil litigation cases into discrete categories can be useful for broad analytical purposes, determining exactly how many cases fall into each group is not so simple. For example, some landlord-tenant disputes involve individual landlords rather than companies, so a subset of cases within that category may not fall under the business-to-consumer umbrella. On the other hand, a large share of cases filed in small claims court are low-dollar-value business-to-consumer lawsuits, but because courts typically do not distinguish small claims by case type, the exact proportion is difficult to determine. Accordingly, Figures 2 and 3 almost certainly understate the share of civil court cases that involve businesses suing individual consumers because it treats small claims as a wholly separate category.

The most recent national data show that, as of 2013, debt collection lawsuits—which most often involve unpaid medical, auto loan, or credit card bills—have become the single most common type of civil litigation, representing 24 percent of civil cases compared with less than 12 percent two decades earlier.11 (See Figure 4.) From 1993 to 2013, the number of debt cases rose from fewer than 1.7 million to about 4 million.12 These figures correspond with an increase in share from an estimated 1 in 9 of 14.6 million state civil cases nationwide (11.6 percent) to about 1 in 4 of 16.9 million cases (23.6 percent)13. Further, in a national survey by the Consumer Financial Protection Bureau (CFPB), nearly 1 in 20 adults with a credit report reported having been sued by a creditor or debt collector in 2014.14

Notably, the 2013 data show that 75 percent of civil case judgments were for less than $5,200,15 which means that in most states, debt claims are typically filed in a limited or small claims court. In fact, NCSC observed in 2015 that small claims courts “have become the forum of choice for attorney-represented plaintiffs in lower-value debt collection cases.”16 As was the case for the business-to-consumer cases shown in Figure 3, the data in Figure 4 probably undercount debt claims because they do not include any debt collection cases filed in small claims court.

Only a few state courts have consistently reported data on debt claims since 2013, but the available information indicates that these lawsuits continue to dominate court dockets. For example, in 2018, the number of debt collection lawsuits filed across all Texas courts was more than twice what it was in 2014.17(See Figure 5.) The state’s small claims courts—known as justice courts—alone experienced a 140 percent increase in debt cases over that five-year period.18 In total, collectors filed one debt claim for every 19 adults in the state over that span.19

Similarly, Alaska’s District Court, which tries all civil matters in the state for values of $100,000 or less, heard 48 percent more debt claims in fiscal year 2018 than 2013.20

Pew found that in 2018, only 12 states—Alaska, Arkansas, Colorado, Connecticut, Missouri, Nevada, New Mexico, Texas, Utah, Vermont, Virginia, and Wyoming—reported statewide debt claims caseload data for at least one of their courts on their public websites.21 Virginia, for instance, reports debt claims data for the state’s district courts—which hear cases with values up to $25,000—but not the circuit courts, which hear cases with values of $4,500 and up.22 Despite these differences, debt claims are consistently among the most common types of cases in the courts that report relevant information. (See Figure 6.) However, in light of the limited number of states and courts reporting, more data and research are needed to gain a complete picture of what is happening nationwide and state by state.

Factors Contributing to the Rise of Debt Claims

The increase in debt claims parallels two major national trends: a rise in household debt and the emergence of the debt-buying industry.

Americans’ household debt nearly tripled from $4.6 trillion in 1999 to $12.29 trillion in 2016, roughly overlapping with the period of rapid growth in debt collection litigation.23 Further, as of 2018, an estimated 71 million people—nearly 32 percent of U.S. adults with a credit history—had debt in collections reported in their credit files, and 1 in 8 households across all income levels had a problem or dispute related to debt, credit, or loans.24

Most household debt in collection stems from a financial shock, such as a job loss, illness, or divorce, and reflects the broader financial fragility of many American households. Nationwide, 2 in 5 adults say that, without selling personal property or borrowing the money, they would not have enough cash to cover an emergency expense costing $400,25 and 1 in 3 families report having no savings.26 Medical debt can be particularly devastating and accounts for more than half of all collections activity.27

Unsurprisingly, low- and moderate-income Americans are disproportionately affected by debt collection. A 2017 CFPB survey found that people in the lowest income bracket were three times as likely as those in the highest income group to have been contacted about a debt in collection and that people with lower incomes also were more likely to have been sued for a debt.28

Creditors who pursue consumer debts into collection include banks and credit unions, hospitals and other medical providers, utility companies, telecommunications companies, auto and student lenders, and, increasingly, debt buyers—firms that purchase defaulted debts from the original creditors at a fraction of the face value, sometimes less than one cent on the dollar, and then attempt to collect on the full amount owed.29

Debt buyers are key figures in many debt collection lawsuits and may have played a significant role in the rise of civil debt cases. During the same 20-year time frame that debt claims increased, 1993 to 2013, the total dollar value of debts purchased by debt buyers grew from $6 billion to $98 billion.30 (See Figure 7.)

Debt buyers employ various collection methods, but studies show that they are increasingly relying on litigation.31 Two of the largest publicly traded debt buyers, Encore Capitol and Portfolio Recovery Associates, saw their legal collections grow 184 percent and 220 percent, respectively, from 2008 to 2018.32

As a result, debt buyers are among the most active civil court users, and in some states, a small number of debt buyers account for a disproportionate percentage of civil cases filed. For example, in Massachusetts, nine debt buyers represented 43 percent of civil and small claims caseloads in 2015, and in Oregon, six debt buyers accounted for 25 percent of all civil cases from 2012 to 2016.33

Courts are not designed to respond to the realities of debt claims

Although civil court dockets have changed, the rules they operate on have largely stayed the same. Courts expect both parties to mount a case and present legal arguments so that the judge can make a decision based on the facts.

However, that is not how today’s debt collection lawsuits play out.

Debt claim defendants rarely have legal representation

The U.S. Constitution provides the right to an attorney for most criminal defendants regardless of ability to pay,34 but that right extends to people being sued in civil court only in very limited instances. Instead, civil case litigants on both sides must pay for their own representation, and data show that such representation is on the decline, especially for those being sued. NCSC found that from the 1990s to 2013, the share of general matters cases in which both sides had a lawyer dropped by more than half, from 96 percent to 45 percent.35

In business-to-consumer suits, and especially debt collection cases, most plaintiffs can afford an attorney, and filing multiple lawsuits in a single court can lower the cost per lawsuit filed. Consumers, however, typically have legal representation in less than 10 percent of debt claims. Studies from 2010 through 2019 show that the share of debt claim defendants who were served—that is, provided with official notification of the suit against them—who had an attorney ranged from 10 percent in Texas to zero in New York City.36 (See Figure 8.)

These low representation rates have real-world implications. Without representation, consumers are unlikely to know their full range of options or recognize opportunities to challenge the cases against them.

For example, every state has a statute of limitations for debt collection lawsuits, ranging from three years in Mississippi to 10 in Rhode Island.37 These laws create an expiration date after which creditors cannot use the courts to collect on a debt. However, enforcement of that prohibition typically falls on the defendant rather than on the courts. For example, if a plaintiff sues on such an expired debt, also called a time-barred debt, the defendant must raise the question of a statute of limitations in order for the court to consider whether the case is even eligible to be heard. But without professional legal help, most consumers would not have the requisite knowledge to demand that the plaintiff prove that the case was filed in time.

Of course, even defendants with representation may lose in court if the facts favor the plaintiff. However, analyses from jurisdictions across the country indicate that when consumers are represented by attorneys, they are more likely to secure a settlement or win the case outright.38 For example, a study of nearly 297,000 debt cases in Virginia district and circuit courts disposed between April 2015 and May 2016 found that debt cases were more likely to be dismissed if defendants were represented by an attorney.39 Similarly, a study of over 165,000 debt cases disposed in Utah from 2015 to 2017 found that 53 percent of represented defendants won their cases, compared with 19 percent of those without representation.40

These data indicate that the absence of legal counsel can have serious repercussions for defendants in consumer debt claims. The problem has become sufficiently widespread that in 2016, the Conference of Chief Justices (CCJ) and Conference of State Court Administrators’ (COSCA) Civil Justice Improvement Committee declared that lack of representation among defendants is “creating an asymmetry in legal expertise that, without effective court oversight, can easily result in unjust case outcomes.”41

Debt lawsuits frequently end in default judgment, indicating that many people do not respond when sued for a debt

Why do so few consumers in debt claims have lawyers? One reason is the prohibitive cost of a lawyer. But another, indicated by the outcome of large shares of debt collection cases, is that many consumers do not participate in the lawsuit at all.

Courts are designed to allow the opposing sides to present legal arguments and facts to support their positions, after which the judge, acting as a neutral arbiter, makes a decision based on that information.

What Are the Steps of a Debt Claim?

In most civil cases, the parties follow the state’s civil procedure:42

Plaintiff (e.g., creditor or debt buyer) files a complaint in court and provides notice of the lawsuit to defendant (i.e., person being sued).

Defendant responds with a written answer. If the defendant does not respond, the court issues a default judgment for the plaintiff.

The two parties exchange documents, including discovery (questions and requests for information) and pleadings (written motions and other legal maneuvers).

Court holds one or more hearings and possibly a trial. If a trial is held, parties can present evidence to a judge or jury.

Judge issues a ruling, which either party may appeal.

A judge presides over the hearings and possible trial, but the litigants manage nearly every step before that, and court processes, such as scheduling a hearing, are driven by their actions. Parties can also settle the case at any time by, for example, negotiating with each other or working with a neutral mediator.

For low dollar amounts, small claims courts use a different procedure, originally designed to provide streamlined and simplified proceedings, particularly for litigants without attorneys.43 Written answers are optional, rules of evidence do not apply, and in many jurisdictions, the parties have no immediate right to appeal. The common steps are:

Plaintiff files a complaint in court and notifies the defendant about the lawsuit.

Parties come to court for a trial in front of a magistrate or other judicial officer.