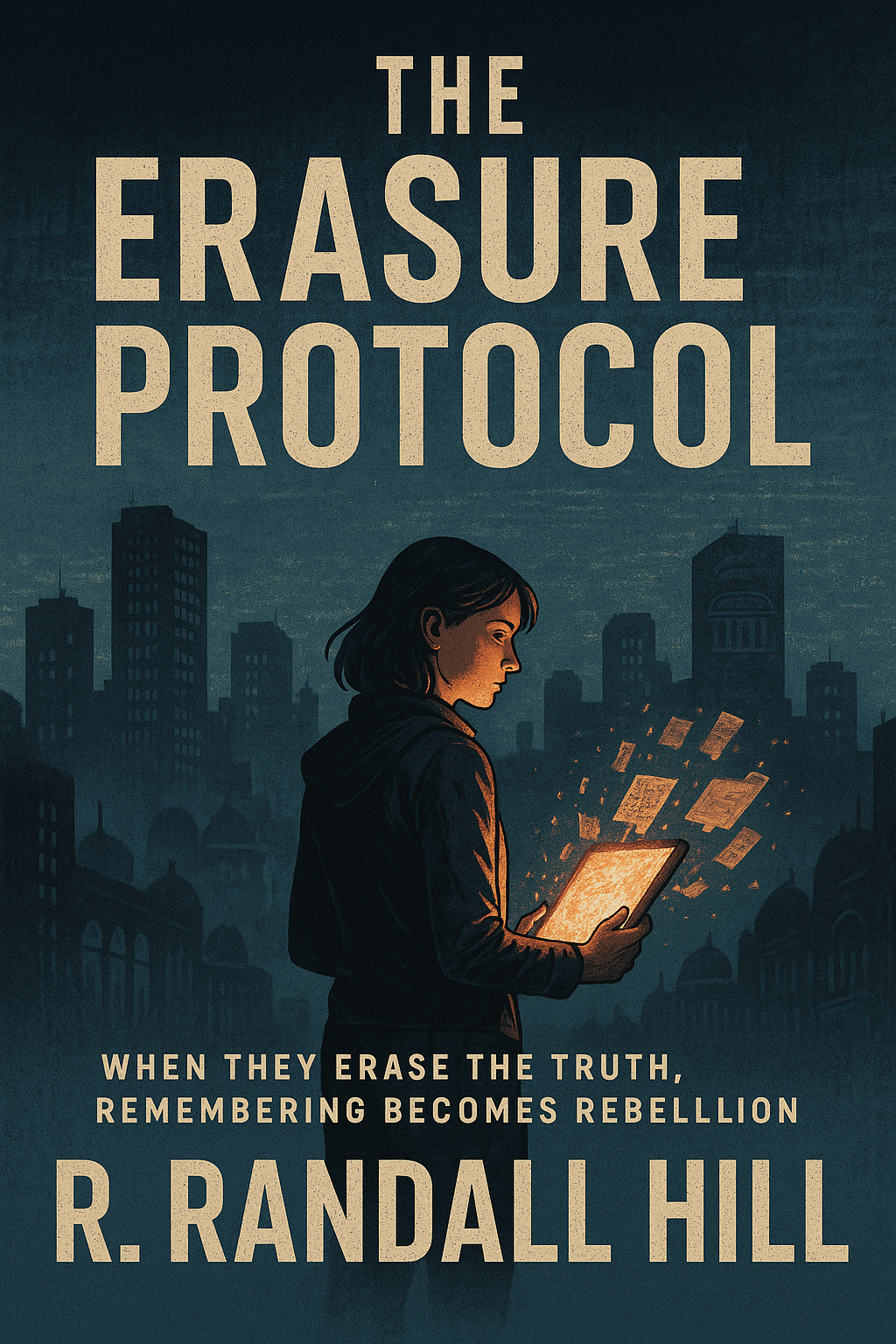

Imagine waking up in a world where schools no longer exist, history books are banned, and even memory is policed. That’s the chilling reality of The Erasure Protocol, the new dystopian novel by R. Randall Hill, author of Legal Research for Non-Lawyers and founder of Court.Rchp.com.

A Glimpse Inside the Story

“When they erase the truth, remembering becomes rebellion.”

In a near-future America where mass education has ended because of AI, citizens are divided into rigid classes:

Dependents, pacified with meaningless “comfort learning.”

Productives, trained only for repetitive labor.

Essentials, groomed to rule.

But one young woman, Maya, refuses to forget. With a hidden tablet and fragments of forbidden knowledge, she discovers that memory itself can be a weapon. As she connects with underground “Memory Keepers,” Maya must risk everything to challenge a system built on ignorance and control.

While fictional, the book is rooted in documented history:

From Roman “bread and circuses,”

To Bacon’s Rebellion,

To slave codes and the systematic exclusion of minorities from education.

These examples show how knowledge has been manipulated to maintain power. The novel’s warning feels urgent today, when schools and libraries face renewed pressure to restrict curricula or sanitize history.

Why This Story Matters Now

At Court.Rchp.com, our mission has always been to empower ordinary citizens with access to legal knowledge. The Erasure Protocol carries that mission into fiction, reminding us that access to truth is never guaranteed—it must be protected.

As the story makes clear: the most dangerous phrase in any language may be “Don’t worry about it.”

A Tribute to Teachers and Knowledge Keepers

This novel is also a tribute to the educators, librarians, and ordinary citizens who preserve and share knowledge, often at great personal cost. They are the heroes who stand between truth and erasure.

About the Author

R. Randall Hill is the author of Legal Research for Non-Lawyers and the founder of Court.Rchp.com, a free self-help legal website. His work is dedicated to empowering ordinary citizens to access knowledge and defend their rights.

Get Your Copy

The Erasure Protocol is available now in PDF, and Kindle formats. Teachers, administrators, and school staff can receive a 50% discount as a thank-you for their dedication to education.

If this story resonates with you, please share this article with a teacher, librarian, parent, or student who believes that education is freedom.

Closing Thought: The most dangerous phrase in any language may be: “Don’t worry about it.” The Erasure Protocol challenges us all to worry about it—to remember, to resist, and to keep the truth alive.

Only “persons” can engage with the legal system – for example, by signing contracts or filing lawsuits. There are two main categories of persons: humans, termed “natural persons,” and creations of the law, termed “artificial persons.” These include corporations, nonprofit organizations and limited liability companies (LLCs).

Up to now, artificial persons have served the purpose of helping humans achieve certain goals. For example, people can pool assets in a corporation and limit their liability vis-à-vis customers or other persons who interact with the corporation. But a new type of artificial person is poised to enter the scene – artificial intelligence systems, and they won’t necessarily serve human interests.

As scholarswho study AI and law, we believe that this moment presents a significant challenge to the legal system: how to regulate AI within existing legal frameworks to reduce undesirable behaviors, and how to assign legal responsibility for autonomous actions of AIs.

This is far from a philosophical question. The laws governing LLCs in several U.S. states do not require that humans oversee the operations of an LLC. In fact, in some states, it is possible to have an LLC with no human owner, or “member” – for example, in cases where all of the partners have died. Though legislators probably weren’t thinking of AI when they crafted the LLC laws, the possibility for zero-member LLCs opens the door to creating LLCs operated by AIs.

Many functions inside small and large companies have already been delegated to AI in part, including financial operations, human resources and network management, to name just three. AIs can now perform many tasks as well as humans do. For example, AIs can read medical X-rays and do other medical tasks, and carry out tasks that require legal reasoning. This process is likely to accelerate due to innovation and economic interests.

A different kind of person

Humans have occasionally included nonhuman entities like animals, lakes, and rivers, as well as corporations, as legal subjects. Though in some cases these entities can be held liable for their actions, the law only allows humans to fully participate in the legal system.

One major barrier to full access to the legal system by nonhuman entities has been the role of language as a uniquely human invention and a vital element in the legal system. Language enables humans to understand norms and institutions that constitute the legal framework. But humans are no longer the only entities using human language.

An LLC established in a jurisdiction that allows it to operate without human members could trade in digital currencies settled on blockchains, allowing the AI running the LLC to operate autonomously and in a decentralized manner that makes it challenging to regulate. Under a legal principle known as the internal affairs doctrine, even if only one U.S. state allowed AI-operated LLCs, that entity could operate nationwide – and possibly worldwide. This is because courts look to the law of the state of incorporation for rules governing the internal affairs of a corporate entity.

We believe the best path forward, therefore, is aligning AI with existing laws, instead of creating a separate set of rules for AI. Additional law can be layered on top for artificial agents, but AI should be subject to at least all the laws a human is subject to.

In addition to embedding law into AI agents, researchers can develop AI compliance agents – AIs designed to help an organization automatically follow the law. These specialized AI systems would provide third-party legal guardrails.

Researchers can develop better AI legal compliance by fine-tuning large language models with supervised learning on labeled legal task completions. Another approach is reinforcement learning, which uses feedback to tell an AI if it’s doing a good or bad job – in this case, attorneys interacting with language models. And legal experts could design prompting schemes – ways of interacting with a language model – to elicit better responses from language models that are more consistent with legal standards.

Law-abiding (artificial) business owners

If an LLC were operated by an AI, it would have to obey the law like any other LLC, and courts could order it to pay damages, or stop doing something by issuing an injunction. An AI tasked with operating the LLC and, among other things, maintaining proper business insurance would have an incentive to understand applicable laws and comply. Having minimum business liability insurance policies is a standard requirement that most businesses impose on one another to engage in commercial relationships.

The incentives to establish AI-operated LLCs are there. Fortunately, we believe it is possible and desirable to do the work to embed the law – what has until now been human law – into AI, and AI-powered automated compliance guardrails.

Republished with permission under license from The Conversation.

They all face racism in the ‘gray areas’ of workplace culture

by Adia Harvey Wingfield, Arts & Sciences at Washington University in St. Louis

American workplaces talk a lot about diversity these days. In fact, you’d have a hard time finding a company that says it doesn’t value the principle. But despite this – and despite the multibillion-dollar diversity industry – Black workers continue to face significant hiring discrimination, stall out at middle management levels and remain underrepresented in leadership roles.

As a sociologist, I wanted to understand why this is. So I spent more than 10 years interviewing over 200 Black workers in a variety of roles – from the gig economy to the C-suite. I found that many of the problems they face come down to organizational culture. Too often, companies elevate diversity as a concept but overlook the internal processes that disadvantage Black workers.

Take “Constance,” for example – not her real name – who is a Black female chemical engineering professor at a major research university. Her university proclaims its commitment to diversity and inclusion, with several offices and initiatives dedicated to this goal.

Yet she told me that most leaders at her school are uncomfortable trying to achieve racial diversity. They’d rather be “colorblind” – that is, they’d rather not acknowledge or address racial disparities or the institutional rules and norms that perpetuate them. So their attempts to pursue diversity translate into attempts to hire more women faculty but not more Black faculty.

This isn’t surprising, as women generally are underrepresented in STEM fields. But the emphasis on gender means that the racial issues Constance encounters as a Black woman – openly racist teaching evaluations, colleagues’ casual stereotyping, additional barriers to mentorship – go ignored.

“Kevin” offers another instructive example. He’s a Black man who works at an education nonprofit that aims to help kids – a laudable goal. His workplace touts its culture of collaboration and says that it demonstrates its commitment to diversity by supporting children from all backgrounds.

But in practice, Kevin found that the organization often shunned and patronized Black parents, treating them disrespectfully. And despite his employer’s stated support for diversity, Kevin says his efforts to highlight these problems usually went ignored.

And then there’s “Brian.” A film producer with extensive Hollywood experience, Brian was excited about taking a job with a major studio. He thought it would give him an opportunity to bring more films about the variety of Black experience to audiences. And since studio leaders talked a big game about innovation, creativity and original thinking, this seemed like a reasonable assumption.

But once he started in this role, Brian learned that the studio was dominated by a market-driven culture, which leaders used to justify not investing in films by and about Black people. Importantly, the same logic around Black filmmakers rarely seemed to apply to white ones, Brian said – those who directed flops were still given multiple chances to keep working. Pointing out this hypocrisy failed to change minds or practices, Brian found.

When a DEI statement isn’t enough

What do these three people, working in very different industries, have in common? They all work for employers that have a stated commitment to diversity – and an organizational culture that belies and even undermines it.

When these companies commit to diversity but fail to tackle racial diversity specifically, it becomes easy for workers like Constance, Kevin and Brian to find that the issues they experience get overlooked and that there’s no effective way to bring them forward. They get stuck in the gray areas.

by Guo Xu, University of California, Berkeley and Abhay Aneja, University of California, Berkeley

Economic disparities in earnings, health and wealth between Black and white Americans are staggeringly large. Historical government practices and institutions – such as segregated schools, redlined neighborhoods and discrimination in medical care – have contributed to these wide disparities. While these causes may not always be overt, they can have lasting negative effects on the prosperity of minority communities.

Abhay Aneja and I are researchers at University of California, Berkeley, who specialize in examining the causes of social inequality. Our new research examines the U.S. federal government’s role in creating conditions of racial inequality more than a century ago. Specifically, we researched the harmful impact of government discrimination against Black civil service employees. We also examined how such discrimination continues to affect their families decades later, rippling across future generations.

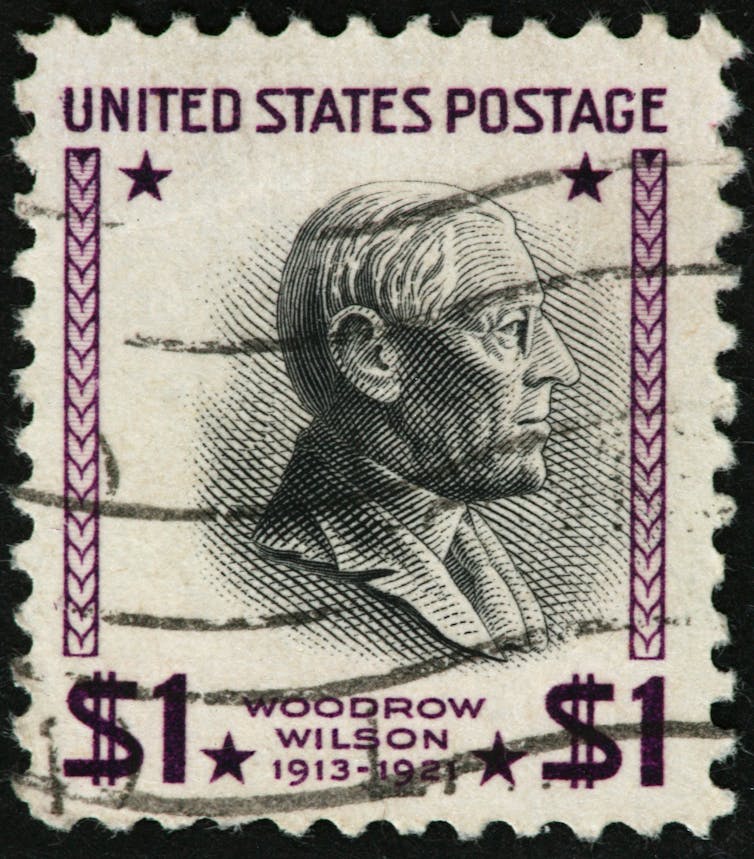

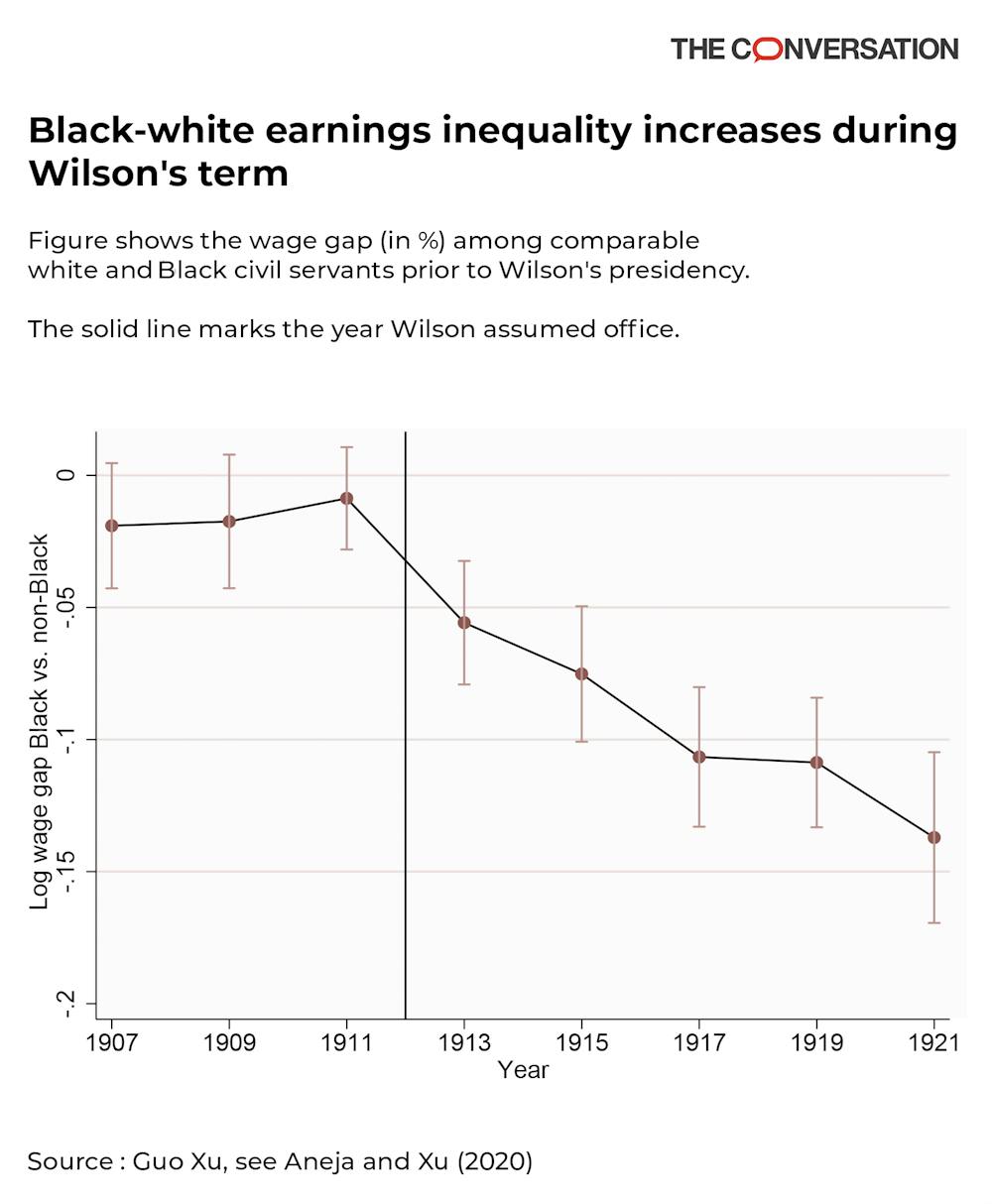

A 1938 stamp honoring former President Woodrow Wilson, considered one of America’s most progressive presidents. iStock / Getty Images Plus

Decades of discrimination

Soon after his inauguration in 1913, President Woodrow Wilson ushered in one of the most far-reaching discrimination policies of that century. Wilson discreetly authorized his Cabinet secretaries to implement a policy of racial segregation across the federal bureaucracy.

A Southerner by heritage, Wilson appointed several Southern Democrats to Cabinet offices, several of whom were sympathetic to the segregationist cause. Wilson’s new postmaster general, for example, was “anxious to segregate white and negro employees in all Departments of Government.” Historical accounts suggest that Wilson’s order was carried out most aggressively by the U.S. Postal Service and the U.S. Treasury Department, the latter responsible for revenue generation including taxes and customs duties. Based on the data we collected, the majority of Black civilians worked in these two federal departments before Wilson’s arrival.

Given his support among Southern Democrats, one goal of the Wilson administration was to limit the access of Black civil servants to the highest positions within government. This outcome was achieved through both demotions and reductions, efforts to discourage the hiring of qualified Black candidates.

For example, photos became required to apply for government jobs in order to screen out Black candidates. Black Americans already employed in the federal civil service were transferred from relatively high-status posts to low-paying ones. This overall policy of Jim Crow-style segregation served to shut out Black Americans from working in one of the few places where they could find opportunities for economic mobility and success.

Deep roots of economic disparities

Despite the potential for enormous harm, the cost of segregation to the economic status of Black civil servants has long remained unknown. Our research started by examining how President Wilson contributed to earnings disparities between Black and white civil service workers. In so doing, our research added to the collective knowledge within the social sciences about the roots of racial inequality.

To build a database on earnings inequality, our team undertook a large-scale data digitization of previously undigitized and, to our knowledge, unexamined historical government records containing a detailed list of all people who worked for the federal government and what they earned each year. These records were contained in eight volumes of the Official Register of the U.S., a series spanning 1907 to 1921. For 1907, we obtained information for 125,000 workers. By 1921, the size of the government workforce had more than doubled.

This data collection and cleaning process created a comprehensive dataset to understand the operation of the American federal government at the beginning of the 20th century. It not only described a worker’s position and salary, but also contained rich personal information including a federal employee’s place of birth, the state from which they were appointed and the Cabinet department where they worked.

Because the register was issued every two years, our research made it possible to track a civil servant’s career progression over time. Looking at this data source, it was clear that President Wilson’s policy of segregating the federal workforce exacted an enormous cost from Black civil servants.

Sidelining Black federal workers

To isolate the impact of racial discrimination and establish comparable jobs and salaries, the analysis paired Black and white federal employees with similar characteristics. Each worked in the same city, the same government office and even had the same salary before President Wilson’s inauguration. Within this set of comparable workers, Black civil servants earned about 7% less than their white counterparts during Wilson’s two terms as president.

When we account for differences in civil servants, such as educational background, the reduction in earnings suffered by Black civil servants remains. Moreover, under the order to segregate, Black civil servants were less likely to be promoted over time and more likely to be demoted. This disparate treatment by the federal government enabled white civil servants to earn more over time than Black civil servants with the same levels of skill and experience. Our research provides strong evidence for the discriminatory nature of workplace segregation faced by Black Americans within the federal government.

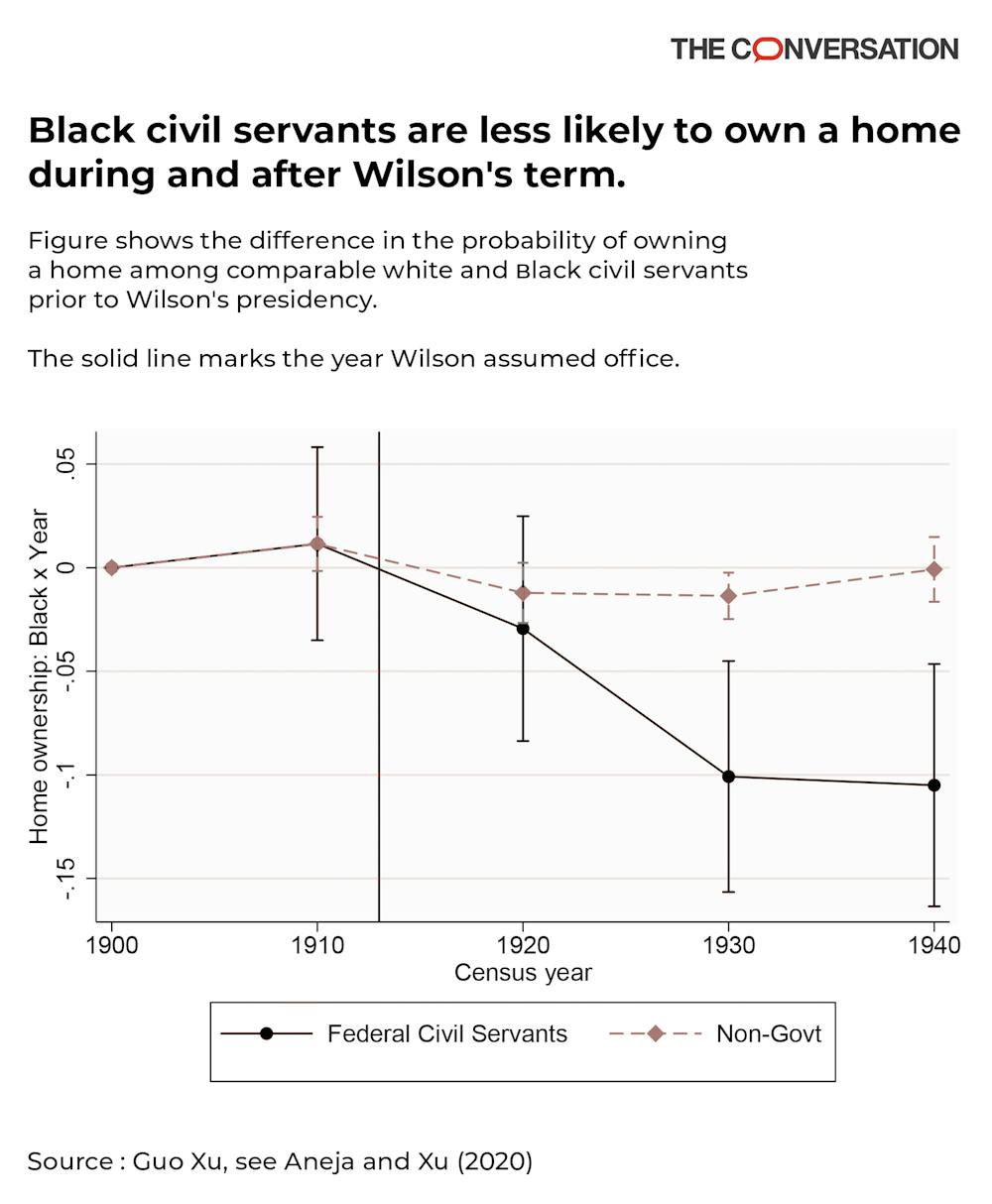

Black workers targeted by federal policies earned less money and had less capacity to own a home.Figure by Aneja and Xu (2020)

Our research shows that the damage caused by working under discriminatory conditions persisted well beyond Wilson’s presidency. The same Black civil servants victimized by discrimination in federal employment were also less likely to own a home in 1920, 1930 and 1940, almost three decades after Wilson was elected. Moreover, the school-age children of Black civil servants who served in the Wilson administration went on to have poorer-quality lives than their young white counterparts in terms of their overall earnings and quality of employment in adulthood.

This research can help to contribute to the understanding of the roots of economic disparities. A policy of racial discrimination – even if implemented temporarily – has lasting negative effects. A clearer understanding of historical discrimination can help to inform the design of policies aimed at remedying the painfully persistent racial inequities we observe today.

Republished with permission under license from The Conversation.

The potential impact that having fewer prisoners to draw upon highlights the crucial role that incarcerated workers play in disaster response. While many people are aware that prisoners work to help contain wildfires in California and elsewhere, less well known is the role incarcerated workers play as a labor source across a variety of disasters throughout the country.

As a social scientist, I study the impact of disasters on incarcerated populations. I recently co-authored a study on the role of incarcerated workers in state emergency operations plans – the primary emergency planning documents for state governments. We found that 30 out of the 47 states analyzed, including California, Texas and Florida, had explicit instructions to use prisoners for emergencies and disasters. Furthermore, we identified at least 34 disaster-related tasks that states assign to incarcerated workers. Delaware, New Jersey and Tennessee were not included in our analysis as their plans were not publicly available.

These include work that requires minimal training such as making sandbags, clearing debris, handling supplies and caring for pets for evacuees. But it also includes roles that require specialized training like fighting fires, collecting and disposing contaminated animal carcasses and cleaning up hazardous materials.

Some of these tasks put incarcerated workers at risk of injury or ill health.

Prisoners clearing vegetation to prevent the spread of a wildfire in Yucaipa, California. David McNew/AFP via Getty Images

14 cents an hour

Prison systems have long championed the work of incarcerated persons in emergencies and disasters as a demonstration of the value of prisons to local communities and the state.

State prison systems often have internal policies that guide the use of incarcerated persons to assist with disaster operations. For example, the Alabama Department of Corrections’ administrative regulations dictate that in the event of a disaster, “the major support of the [department] will be manpower” including the use of “inmate labor.”

In addition, state laws across the U.S. often specifically state that incarcerated workers may be assigned to work in disaster conditions.

For example, Georgia allows for incarcerated workers to be required to work in conditions that may jeopardize their health if an emergency threatens the lives of others or of public property. Meanwhile Colorado passed legislation in 1998 that created the Inmate Disaster Relief Program under which the state can “form a labor pool” to “fight forest fires, help with flood relief, and assist in the prevention of or clean up after other natural or man-made disasters.”

As with wildfire programs, incarcerated workers are looked to in times of disaster primarily because they are a low-cost substitution for civilian workers. Incarcerated workers are paid very low wages averaging between US$0.14 and $0.63 an hour. And some states, including Alabama, Arkansas, Florida, Georgia and Texas, don’t pay incarcerated workers at all.

The cost of inmate labor is offset through federal subsidies. FEMA’s public assistance program provides states with “funding for prisoner transportation to the worksite and extraordinary costs of security guards, food and lodging.” This provides a significant financial incentive to use incarcerated workers for disaster labor. After Hurricane Michael in 2018, FEMA awarded the Florida Department of Corrections $311,305 for debris removal.

Forced labor

Not all disaster work is voluntary for incarcerated persons. The 13th Amendment to the U.S. Constitution allows for incarcerated persons to be compelled to participate in labor without their consent as part of their punishment. That applies to disaster work too.

The Constitution’s Eighth Amendment “forbids knowingly compelling an inmate to perform labor that is beyond the inmate’s strength, dangerous to his or her life or health, or unduly painful.” However, in the context of disasters, it is challenging to know whether or not the situation or the environment is truly safe. And little is known about the training prisoners receive.

If incarcerated persons refuse to participate, they may face serious consequences, such as being sent to solitary confinement, the loss of earned time off their sentences or the loss of family visitation.

Deaths of incarcerated firefighters are reported alongside those of civilian firefighters, and there is no way to accurately track the number of prisoners who have died or been injured during disaster-related work. However, there are known examples of fatalities. In 2003, the South Dakota Department of Corrections “Emergency Response Inmate Work Program” was scrutinized after a 22-year-old man, Neil Ambrose, was electrocuted by a downed power line while cleaning up debris after a storm.

Ambrose reportedly expressed prior concerns about the hazardous work but was told he would be charged with “disrupting a work zone” and would be sent to solitary confinement if he did not participate. Later, the correctional officer in charge of Ambrose and those on the work crew was found responsible for his death in that he knew the downed power line was a safety threat. It was also later shown that the only training Ambrose had received was a short video on safely operating chainsaws.

Exploitation and harm

Some advocates for prisoners’ rights have begun drawing attention to the vulnerability of incarcerated workers in disasters. After Hurricane Harvey in 2017, the NAACP Environmental and Climate Justice program published a guidebook called “In the Eye of the Storm” to help communities make disaster response and recovery processes more equitable. The guidebook includes suggestions for how to advocate specifically for worker protections for incarcerated persons. Community members are encouraged to ask about whether the incarcerated workers have received relevant training and adequate protective equipment and if their participation in the work is voluntary.

Incarcerated workers are deeply embedded throughout emergency management in the United States. Yet so much attention remains focused on the most visible and well-known programs, their role – and the potential for exploitation and harm – in many other disasters remains overlooked.

Republished with permission under license from The Conversation.

The job of slicing up the economic pie in the U.S. has traditionally fallen to Congress, with the Federal Reserve tasked with making sure there is enough to go around. But this could soon change.

Under proposals put forward by Democrats in Congress, the mandate of the Fed would be tweaked for the first time since 1977, when its objectives were made explicit: promote maximum employment, stable prices and moderate long-term interest rates. Under the new proposals, the central bank would gain an additional task of reducing racial inequality. In short, the central bank could be handed the pie cutter and told to make sure everyone gets a fair share.

A Black Lives Matter protester outside the Federal Reserve Bank in New York. Tayfun Coskun/Anadolu Agency via Getty Images

1. Targeting Black unemployment

The main tool the Fed has in guiding the U.S. economy is through the setting of interest rates. Adjusting its benchmark interest rate changes the cost of borrowing for companies and consumers, which in turn can stimulate or subdue their spending. When the unemployment rate is extremely low – as it was prior to the pandemic – the Fed may increase interest rates. This puts a brake on private consumption and investment and protects against inflation.

The problem is that currently the Fed focuses on the national jobless rate, the same one reported every month in the news. This figure obscures the wide variation among different regions and demographic groups, not to mention it ignores the growing share of Americans who are underemployed.

At present, the Fed uses the national unemployment rate to help guide its rate setting. But even during times of prosperity, the Black American jobless rate is roughly two times the white rate. As a result of the Fed targeting the national unemployment rate – which is roughly equal to the white rate – interest rates are hiked before many Black Americans fully experience the benefits of a deep and lengthy economic boom. My research with former Fed economist Seth Carpenter shows that when the Fed puts its foot on the brakes, the Black jobless rate rises more. Black teen unemployment suffers the most from this brake pumping.

But in line with a change to the mandate to include reducing racial inequality, central bankers could ditch the national rate as its target and instead use the Black unemployment rate. Doing so would still maintain strong economic growth for white Americans but would enable the Fed to set rates in a way tailored to addressing the economic needs of Black people too.

2. Opening up credit

The Fed can also use tools handed to it under the Community Reinvestment Act to narrow racial wealth differences and provide Black Americans with greater access to credit. The act, enacted in 1977, requires the Fed to use its oversight powers to encourage financial institutions to help meet the credit needs of the communities in which they do business, particularly in low- and moderate-income neighborhoods. The new proposals specifically call on the Fed to aggressively implement the act.

This is important because many Black consumers continue to experience discrimination getting loans and mortgages.

3. Reporting discrimination

Proposals in the act would ensure that policymakers and the public are made fully aware of racial economic disparities. Under the act’s terms, the Fed would be required to report on recent racial, ethnic, gender and education gaps in income and wealth, with the Fed chair expected to identify racial disparities in the labor market through periodical congressional testimony. The chair would also have to make public how the Fed intends to reduce these gaps.

This is important because the act could be viewed as lessening Congress’ traditional role of using fiscal policy such as taxation and spending to address issues of inequality. Instead, the Fed’s new data collection and analysis responsibilities would put additional pressure on lawmakers to act.

I believe this could have a profound long-term impact on not only individual Black families but the national economy as a whole. The availability of much more data that clearly shows just how wide the racial inequality gap is would put pressure on Congress to find ways to help Black Americans accumulate wealth and the means to secure and affordable housing. This would likely result in lower health care costs, increased housing values and lower crime. This in turn could lead to less spending on social services, with savings redeployed to community enterprises that raise overall productivity.

Likewise highlighting racial discrepancies in employment could force Congress to introduce proposals to bring equitable child care and education to Black communities, as well as better transportation and reliable technology, all of which would raise worker productivity.

No silver bullet

Changing the Fed’s remit is no silver bullet. But at a minimum, the provisions of the proposed act – to make reducing inequality part of the Fed’s mission, to ensure that racial economic disparities are not ignored and to require robust reporting on labor force disparities – could provide a federal response to racial disparities that moves the needle on improving the prosperity of Black Americans. And it comes as America’s reckoning with systemic racism has received fresh urgency and scrutiny following the killing of George Floyd.

Despite this fresh impetus, the act faces an uphill battle. It is unlikely to become law under present political circumstances. And even if the Democrats succeed in winning the Senate and presidency in November, the chances for the act’s success are uncertain. But if over time more Fed governors are appointed that support the proposed mandate, the act’s elements could become policy and practice. This updated mandate would represent a down payment by one of the nation’s most powerful institutions to end systemic racism.

by Paige Marta Skiba, Vanderbilt University; Dalié Jiménez, University of California, Irvine; Michelle McKinnon Miller, Loyola Marymount University; Pamela Foohey, Indiana University, and Sara Sternberg Greene, Duke University

As more Americans lose all or part of their incomes and struggle with mounting debts, another crisis looms: a wave of personal bankruptcies.

Bankruptcy can discharge or erase many types of debts and stop foreclosures, repossessions and wage garnishments. But our research shows the bankruptcy system is difficult to navigate even in normal times, particularly for minorities, the elderly and those in rural areas.

COVID-19 is exacerbating the existing challenges of accessing bankruptcy at a time when these vulnerable groups – who are bearing the brunt of both the economic and health impact of the coronavirus pandemic – may need its protections the most.

If Americans think about turning to bankruptcy for help, they will likely find a system that is ill-prepared for their arrival.

The courts are sheltering in place too.

It’s a hard road

There are many benefits to filing bankruptcy.

For example, it can allow households to avoid home foreclosure, evictions and car repossession. The “automatic stay” triggered at the start of the process immediately halts all debt collection efforts, garnishments and property seizures. And the process ends with a discharge of most unsecured debts, which sets people on a course to regain some financial stability.

We know from our empirical research, however, that filing for bankruptcy comes with costs. In a Chapter 7 case, known as a liquidation when a debtor’s property is sold and distributed to creditors, households may be required to surrender some of their assets. The post-bankruptcy path to financial stability is often bumpy.

Nonetheless, struggling Americans may find bankruptcy one of few viable options to address their worsening money problems, particularly as the pandemic shows no signs of ending soon.

In the last 10 days of March, when states began issuing such orders, we found that Chapter 13 filings fell 45% compared with the last 10 days of March 2019, based on a docket search on Bloomberg Law. Filings in all of April – when most states were under lockdown – plunged 60%, while Chapter 7 filings were down 40%.

This suggests that there’s pent-up demand for bankruptcy protection – in terms of what we’d normally expect – on top of the impact from the coronavirus recession.

In somedistricts, only attorneys can file electronically, so people handling the process themselves must mail in their petition or find some other way of getting it to the courts, such as via physical drop boxes.

But such methods still assume access to technology. A computer, the internet and a printer are needed to access and print the petition. Libraries and other institutions that traditionally provide technology access for those who do not have it are, for the most part, closed.

Some courts are allowing initial email submission of the petition from those without attorneys, but petitioners are still required to follow up by sending original documents via the mail or drop boxes. Access to a computer, the internet and a printer remains necessary.

Finally many states require “wet signatures” on bankruptcy petitions. That is, people have to sign their names in ink, as opposed to using an electronic signature. To smooth filings while courts are physically closed, several states have waived this requirement for those using an attorney.

But even then, access issues still abound. People must first send their attorney the vast array of documents needed for filing – typically amounting to dozens of pages. Filers still need to be able to copy, scan and email documents. For those without computer access, they have to mail original documents, a somewhat risky proposition when important papers could get delayed, stolen or lost.

A bad time to file

In other words, the middle of a pandemic is not the best time to file for bankruptcy.

But a first priority should be shoring up individuals, for whom bankruptcy is seen as a last resort. If more aid isn’t forthcoming, the bankruptcy system may be too overwhelmed to handle even that.

The legislation is an emergency intervention to provide paid leave and other support to millions of workers sidelined by school closures, quarantines and caregiving.

An obvious question you’re probably wondering is, “How will it affect me?”

The bad news is that the law does not provide blanket coverage for all workers. Instead, it’s a confusing mess – legislative Swiss cheese, full of exceptions and gradations that affect whether you are covered, for how long and how much pay you can expect to receive.

With schools closed, parents such as Jennifer Green, left, and Lisa Spalding, right, must stay at home with their children. Suzanne Kreiter/The Boston Globe via Getty Images

I study employment law and have combed through the bill to make sense of it. The law also provides emergency funding for unemployment insurance and subsidizes some employer health care premiums, but my focus here is on the core elements pertaining to sick and family leave.

Here’s what I learned.

Small, medium or large

To figure out whether you are covered, the first thing you’ll need to answer is how many people work at your company.

If your employer has 500 or more workers, it is excluded from the new law. Instead, workers at those companies will need to rely on any remaining sick leave benefits available under company policy or state law.

Several states, including New York, California and Washington, are also considering emergency legislation tied to the coronavirus pandemic and may offer some relief for workers at these bigger companies. These workers can also make use of the 1993 Family and Medical Leave Act, which provides for unpaid leave if the employee or a family member falls seriously ill.

In addition, some large employers have made new accommodations for their workers. Walmart, the nation’s largest employer, for example, has extended its sick leave benefits for hourly workers. And coffee chain Starbucks expanded its existing sick leave policy to provide paid leave of up to 26 weeks if an employee contracts COVID-19 and is unable to return to work.

If your company employs fewer than 500 people, you should be covered by the new law. But there’s another exception: Businesses with fewer than 50 employees can make use of a hardship exemption if providing leave might put them out of business.

School closures

Assuming your company is covered, the amount of leave available – and how much workers can expect to get paid – will depend on the reason you aren’t able to report to work or do your job remotely.

Here’s where it gets really complicated.

If you are stuck at home due to the closure of a child’s school or day care, you will be eligible for leave under two separate parts of the new law – paid sick leave and family and medical leave.

Congress seems to have structured the law to allow working parents sidelined by a school closure to use both forms of leave at once. Parents would request up to 12 weeks of leave as family and medical leave for a school closure. But since this part of the law doesn’t offer pay until the third week, parents could use the new sick leave provisions to receive income for the first two weeks.

Whether you’re using sick or family leave, you can expect to receive two-thirds of your usual pay, or up to US$200 per day. The money would come directly from your employer who will be reimbursed by tax credits.

Alternatively, people could use the sick leave for the first two weeks and then take 12 weeks under family leave, for a total of 14 weeks, but that would include two weeks that are unpaid.

If you have any available vacation or sick pay under your company’s policy, you may want to use that first since it typically provides full pay.

What happens if you get sick

Workers who are directly affected by the new coronavirus can expect more generous income replacement – but only briefly.

If you are under government-ordered quarantine or isolation, self-isolating at the instruction of a health care provider or experiencing COVID-19 symptoms and seeking a medical diagnosis, you can make use of the new federal sick leave law for up to two weeks. During this time, you should receive your usual pay, capped at $511 per day.

If you become seriously ill beyond two weeks, the new law does not offer additional paid leave. However, you may be eligible to take another 12 weeks of unpaid leave under the 1993 Family and Medical Leave Act. This covers only companies with more than 50 people and workers employed there for longer than 12 months. During this time, your job is protected, but you may be required to use any accrued sick leave or vacation available under company policy.

The rules are similar if you are caring for someone who is under government-ordered quarantine or isolation or has been ordered to self-isolate by a health care provider. The only difference is that your income would be only two-thirds of your usual pay, capped at $200 a day, for two weeks.

And again, if you are caring for a family member who becomes seriously ill, you may be able to take up to 12 weeks of unpaid leave under the 1993 act without losing your job.

In normal times, legislation like this would have been considered broad and ambitious, but as the crisis deepens, its exclusions will likely leave vulnerable workers exposed. With another stimulus bill in the works, Congress will have another chance to help Americans whose lives have been turned upside down by this pandemic.

Republished with permission under license from The Conversation.

Job prospects for young men who only have a high school diploma are particularly bleak. They are even worse for those who have less education. When young men experience joblessness, it not only threatens their financial well-being but their overall well-being and physical health.

Could a high quality and specialized technical education in high school make a difference?

Based on a study I co-authored with 60,000 students who applied to the Connecticut Technical High School System, the answer is: yes.

Students in the electrical program at H.C. Wilcox Technical High School in Meriden, Connecticut practice their skills. Connecticut Technical Education and Career System

To reach this conclusion, we studied two groups of similar students: Those who barely were admitted to the Connecticut Technical High School System and those who just missed getting in. Students apply to these high schools and submit things such as test scores, attendance and discipline records from middle school. Then, applicants are ranked on their score and admitted in descending order until all seats are filled. We compared those whose score helped them get the last space in a school, to those who just missed being admitted because the school was out of space.

This enabled us to determine whether there was something special about Connecticut’s Technical High School System education that gave students an advantage over peers who also applied, but didn’t get into one of the system’s 16 technical schools across the state.

Widespread appeal

Connecticut Technical High School System is a popular choice for students – about 50% more students apply than can be admitted.

Students in the Precision Machining program at Vinal Technical High School in Middletown, Conn., gather around their teacher for instruction.Connecticut Technical Education and Career System

The system functions such that students can apply to attend a school in the tech system instead of their assigned public school. Statewide, the system schools – which offer specialized instruction in a variety of career fields – serve about 10% of the high school students. Most students who don’t get into the tech schools stay in their public high school.

What we found is that students who were admitted to the Connecticut Technical High School System went on to earn 30% more than those who didn’t get admitted. We also found that the tech school students were 10 percentage points more likely to graduate from high school than applicants who didn’t get in – a statistically significant finding.

Our research suggests that expanding a technical high school system like the one in Connecticut would benefit more students. I make this observation as one who examines outcomes associated with career and technical education.

The track record

Career and technical education has already been shown – at least on an individual or small scale level – to positively impact earnings and high school graduation rates.

Career and technical education does this without taking away from general learning in traditional subjects like math and English. But based on my experience, it has never been clear as to whether career and technical education makes a difference on a system-wide level rather than at just one or among a few select schools.

Our recent study finally answers that question because we studied an entire state technical high school system. Specifically, it shows that, yes, career and technical education can give students the same benefits that it has already been shown to give on a smaller level even if it’s scaled up. This has implications for school districts and states, especially as growing interest in what works in career and technical education.

The appeal of technical education in Connecticut

Once admitted into the Connecticut technical high school system, all students take career and technical education coursework instead of other electives, such as world languages, art or music. Typically, coursework is grouped into one of 10 to 17 programs of study, such as information technology, health services, cosmetology, heating ventilation and air conditioning, and production processes, among others. Traditional public high schools in the state, on the other hand, tend to offer at most four career and technical programs through elective courses.

In the Technical High School System schools in Connecticut, students explore various programs of study during their first year. Then – with help from an adviser – students select a program of study. Within these programs, students take at least three aligned courses and often more. They also have more opportunity to align academic and technical coursework materials, so that math and English content can often be integrated into technical courses. Chances for work-based learning and job exposure can also be enhanced in these settings, which may contribute to their impact.

Better outcomes

To figure out if these technical schools were making a difference, we looked at admissions from 2006-2007 through 2013-2014 for 60,000 students.

We found that – compared to students who just missed being admitted – technical high school students had:

• Higher 10th grade test scores (like moving from the 50th to the 57th percentile, which is a significant jump for high school test scores)

• A greater likelihood of graduating from high school, about 85% versus 75% for those who just missed being admitted

• Higher quarterly earnings, over 30% higher

• While we found a lower likelihood of attending college initially, no differences were seen by age 23

As educators, elected officials and parents search for more effective ways to give young men in high school a better shot at being able to earn a living, our study suggests that Connecticut might have already figured it out.

Republished with permission under license from The Conversation.

Two years ago, ProPublica and The New York Times revealed that companies were posting discriminatory job ads on Facebook, using the social network’s targeting tools to keep older workers from seeing employment opportunities. Then we reported companies were using Facebook to exclude women from seeing job ads.

Experts told us that it was most likely illegal. And it turns out the federal government now agrees.

A group of recent rulings by the U.S. Equal Employment Opportunity Commission found “reasonable cause” to conclude that seven employers violated civil rights protections by excluding women or older workers or both from seeing job ads they posted on Facebook.

The agency’s rulings appear to be the first time it has taken on targeted advertising, the core of Facebook’s business. “It answers the question from the EEOC’s perspective,” former agency commissioner Jenny R. Yang said. “If you’re excluding older workers from seeing your ads for jobs it does violate” anti-discrimination laws. The EEOC declined to comment.

The decisions stem from complaints filed by the Communications Workers of America, the American Civil Liberties Union and plaintiff’s attorneys after our reporting. The agency made the rulings in July, but they are becoming public now as part of a separate pending class-action suit in federal court accusing companies of age discrimination.

The ads are all from 2018 or earlier. Since then, Facebook has agreed in a settlement to make sweeping changes to the way employers, landlords and creditors can target advertising. The changes are scheduled to take effect by the end of the year.

A Facebook spokesperson pointed to the company’s recent changes and said, “Helping prevent discrimination in housing, employment or credit ads is an area we believe we lead the advertising industry.”

In the latest rulings, the EEOC cited four companies for age discrimination: Capital One, Edwards Jones, Enterprise Holdings and DriveTime Automotive Group. Three companies were cited for discrimination by both age and gender: Nebraska Furniture Mart, Renewal by Andersen LLC and Sandhills Publishing Company. The companies can now work out a settlement with the EEOC or go to court.

Most of the companies did not immediately respond to requests for comment. Nebraska Furniture Mart declined to comment. A spokesperson for financial firm Edwards Jones said, “We strongly disagree with the claim that our firm engaged in discriminatory practices in advertising of job opportunities, recruiting or hiring.”

Dozens of other complaints have been filed with the EEOC about discrimination in targeted advertising on Facebook. Most of the allegations are still pending.

The EEOC’s batch of decisions are significant, attorney Peter Romer-Friedman of Outten & Golden says, because they are the first time companies besides Facebook have had to defend how they use Facebook’s tools to advertise jobs.

His firm also filed a suit against seven real estate companies last week for allegedly discriminating by age in housing ads. We first reported on discriminatory housing ads on Facebook three years ago. The company changed its process for screening housing ads after we retested the system two years ago and showed it was possible to buy dozens of ads that excluded people by gender, race, religion, national origin, age and other categories protected by civil rights laws.

Republished with permission under license from ProPublica.