Lawsuit trends highlight need to modernize civil legal systems

Overview

The business of state civil courts has changed over the past three decades. In 1990, a typical civil court docket featured cases with two opposing sides, each with an attorney, most frequently regarding commercial matters and disputes over contracts, injuries, and other harms. The lawyers presented their cases, and the judge, acting as the neutral arbiter, rendered a decision based on those legal and factual arguments.

Thirty years later, that docket is dominated not by cases involving adversaries seeking redress for an injury or business dispute, but rather by cases in which a company represented by an attorney sues an individual, usually without the benefit of legal counsel, for money owed. The most common type of such business-to-consumer lawsuits is debt claims, also called consumer debt and debt collection lawsuits. In the typical debt claim case, a business—often a company that buys delinquent debt from the original creditor—sues an individual to collect on a debt. The amount of these claims is almost always less than $10,000 and frequently under $5,000, and typically involves unpaid medical bills, credit card balances, auto loans, student debt, and other types of consumer credit, excluding housing (mortgage or rent).

For more than a decade, the American Bar Association and legal advocacy organizations such as the Legal Services Corporation and the National Legal Aid and Defenders Association have sounded alarms about worrisome trends underway in the civil legal system. And court leaders have taken notice. In 2016, a committee of the Conference of Chief Justices, a national organization of state supreme court heads, issued a report recommending that courts enact rules to provide a more fair and just civil legal system, especially with respect to debt collection cases. Chief justices of various supreme courts, with support from private foundations, have established task forces to probe the issue further.

However, until relatively recently, these discussions were largely confined to court officials, legal aid advocates, and other stakeholders concerned about the future of the legal profession. In most states, policymakers have not been a part of conversations about how and why civil court systems are shifting; the extent to which the changes might lead to financial harm among American consumers, especially the tens of millions of people in the U.S. who are stuck in long-term cycles of debt; and potential strategies to address these issues.

To help state leaders respond to the changing realities in civil courts, The Pew Charitable Trusts sought to determine what local, state, and national data exist on debt collection cases and what insights those data could provide. The researchers supplemented that analysis with a review of debt claims research and interviews with consumer experts, creditors, lenders, attorneys, and court officials.

The key findings are:

-

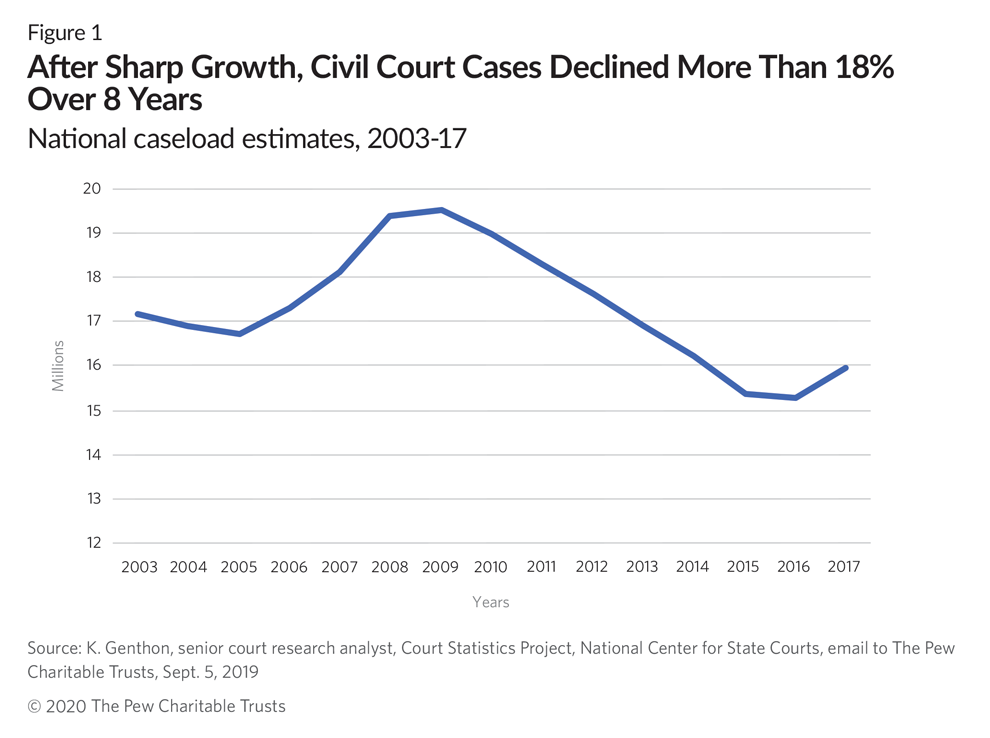

Fewer people are using the courts for civil cases. Civil caseloads dropped more than 18 percent from 2009 to 2017. Although no research to date has identified the factors that led to this decline, previous Pew research shows lack of civil legal problems is not one of them: In 2018 alone, more than half of all U.S. households experienced one or more legal issues that could have gone to court, including 1 in 8 with a legal problem related to debt.

-

Debt claims grew to dominate state civil court dockets in recent decades. From 1993 to 2013, the number of debt collection suits more than doubled nationwide, from less than 1.7 million to about 4 million, and consumed a growing share of civil dockets, rising from an estimated 1 in 9 civil cases to 1 in 4. In a handful of states, the available data extend to 2018, and those figures suggest that the growth of debt collections as a share of civil dockets has continued to outpace most other categories of cases. Debt claims were the most common type of civil case in nine of the 12 states for which at least some court data were available—Alaska, Arkansas, Colorado, Missouri, Nevada, New Mexico, Texas, Utah, and Virginia. In Texas, the only state for which comprehensive statewide data are available, debt claims more than doubled from 2014 to 2018, accounting for 30 percent of the state’s civil caseload by the end of that five-year period.

-

People sued for debts rarely have legal representation, but those who do tend to have better outcomes. Research on debt collection lawsuits from 2010 to 2019 has shown that less than 10 percent of defendants have counsel, compared with nearly all plaintiffs. According to studies in multiple jurisdictions, consumers with legal representation in a debt claim are more likely to win their case outright or reach a mutually agreed settlement with the plaintiff.

-

Debt lawsuits frequently end in default judgment, indicating that many people do not respond when sued for a debt. Over the past decade in the jurisdictions for which data are available, courts have resolved more than 70 percent of debt collection lawsuits with default judgments for the plaintiff. Unlike most court rulings, these judgments are issued, as the name indicates, by default and without consideration of the facts of the complaint—and instead are issued in cases where the defendant does not show up to court or respond to the suit. The prevalence of these judgments indicates that millions of consumers do not participate in debt claims against them.

-

Default judgments exact heavy tolls on consumers. Courts routinely order consumers to pay accrued interest as well as court fees, which together can exceed the original amount owed. Other harmful consequences can include garnishment of wages or bank accounts, seizure of personal property, and even incarceration.

-

States collect and report little data regarding their civil legal systems, including debt cases. Although 49 states and the District of Columbia provide public reports of their cases each year, 38 and the district include no detail about the number of debt cases. And in 2018, only two states provided figures on default judgments in any of their state’s debt cases. Texas is the only state that reports on all types of cases, including outcomes, across all courts.

-

States are beginning to recognize and enact reforms to address the challenges of debt claims. From 2009 to 2019, 12 states made changes to policy—seven via legislation and five through court rules—to improve courts’ ability to meet the needs of all debt claim litigants. Examples of such reforms include ensuring that all parties are notified about lawsuits; requiring plaintiffs to demonstrate that the named defendant owes the debt sought and that the debt is owned by the plaintiff; and in some states, enhanced enforcement of the prohibitions on lawsuits for which the legal right to sue has expired.

Based on the findings of this analysis and these promising efforts in a handful of states, Pew has identified three initial steps states can take to improve the handling of debt collection cases:

-

Track data about debt claims to better understand the extent to which these lawsuits affect parties and at which stages of civil proceedings courts can more appropriately support litigants.

-

Review state policies, court rules, and common practices to identify procedures that can ensure that both sides have an opportunity to effectively present their cases.

-

Modernize the relationship between courts and their users by providing relevant and timely procedural information to all parties and moving more processes online in ways that are accessible to users with or without attorneys.

In 2010, the Federal Trade Commission (FTC) issued a report on the lack of adequate service to consumers in state courts that concluded, “The system for resolving disputes about consumer debts is broken.”1 In the decade since, this problem has not abated and if anything has become more acute. Furthermore, the challenges that this report reviews regarding debt collection cases epitomize challenges facing the civil legal system nationwide. This report summarizes important but inadequately studied trends in civil litigation, highlights unanswered questions for future research, and outlines some initial steps that state and court leaders can take to ensure that civil courts can satisfy their mission to serve the public impartially.

Methods

This study involved a three-step approach to analyze debt collection lawsuit trends in state courts and the significance for consumers. To identify common characteristics and potential consequences of these cases, Pew researchers conducted a literature review of approximately 70 peer-reviewed and gray studies and performed semistructured interviews with experts from state and local courts, consumer advocacy organizations, and the credit and debt collection industries. To analyze the volume of debt claims in the United States and the extent to which courts track and report relevant data, researchers reviewed data from the National Center for State Courts (NCSC), including national caseload statistics from 2003 to 2017 and breakdowns of civil case types in 1993 and 2013, the most recent year for which this level of detail is available. Researchers also collected and analyzed annual court statistical reports for all 50 states and the District of Columbia from 2017 and, where available, from 2005, 2009, 2013, and 2018. Pew researchers conducted quality control for each step to minimize errors and bias. For more information, see the full methodological appendix.

Fewer people are using the courts for civil cases

Beginning in at least the 1980s and continuing through the first decade of the 21st century, caseload volume in civil courts was on an upward trajectory.2 After peaking in 2009, however, it began to decline and by 2017 had dropped to levels not seen in 20 years.3 (See Figure 1.)

Court systems in 44 states, the District of Columbia, and Puerto Rico reported total civil caseloads to NCSC’s Court Statistics Project in 2009 and 2017, and of those, 41 systems described lower caseloads over that span, both in raw numbers and per capita.4

A full examination of drivers of the decline in civil caseloads is outside the scope of this analysis. However, evidence indicates that the drop is not the result of a decrease in legal issues that people could bring to the court. A recent Pew survey found that in 2018, more than half of U.S. households had a legal issue that could have been resolved in court, and that 1 in 4 households had two or more such issues.5;

Civil Courts and Available Data

State courts hear cases in five categories: criminal, civil, family, juvenile, and traffic. For the purposes of this report, and in keeping with the way courts typically divide their dockets, civil cases are organized into five categories:

Debt collection: Suits brought by original creditors or debt buyers claiming unpaid medical, credit card, auto, and other types of consumer debt exclusive of housing (e.g., mortgage or rent).

Mortgage foreclosure: Suits brought by banks and other mortgage lenders seeking possession of a property as collateral for unpaid home loans.

Landlord-tenant: Predominantly eviction proceedings, with a smaller subset of suits brought by landlords for unpaid rent.

Tort: Personal injury and property damage cases; medical malpractice; automobile accidents; negligence; and other claims of harm.

Other: Other contract disputes; real property; employment; appeals from administrative agencies; civil cases involving criminal proceedings;6 civil harassment petitions; and “unknown” cases where the case type was undefined or unclear.

Further, state civil courts are tiered based on the dollar amount of the claims they hear:7

-

General civil matters, characterized by high dollar amounts (minimum value of $12,000 to $50,000, depending on the state; no maximum).

-

Limited civil matters of moderate dollar amounts (minimum value of zero to $10,000 and maximum of $20,000 to $100,000, depending on the state).

-

Small claims with the lowest dollar amounts (no minimum value; maximum of $2,500 to $25,000, depending on the state).

State laws dictate the jurisdiction—city, county, state, etc.—in which a plaintiff can file a suit and, based on the dollar amount of the claim, the tier of court appropriate to the claim. Courts that disaggregate their data in annual statistical reports typically report on claims filed in the general and limited civil courts based on the above five case types (or some variation). However, most states do not disaggregate information on claims filed in small claims jurisdiction courts.

Most civil cases today are brought by businesses against individuals for money owed

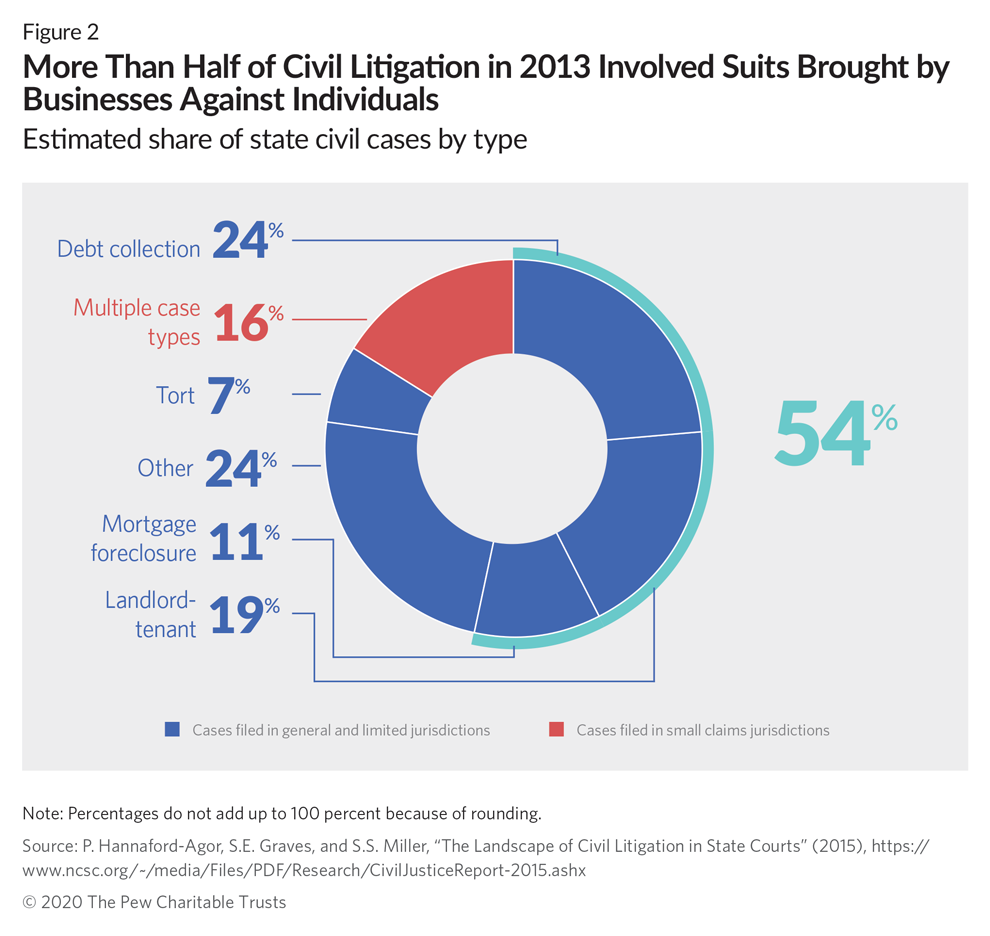

The most recent national data available show that, as the overall volume of cases has declined, business-to-consumer suits, particularly debt collections, mortgage foreclosure, and landlord-tenant disputes, have come to account for more than half of civil dockets.8 (See Figure 2.) As a committee of the Conference of Chief Justices put it in 2016, “Debt collection plaintiffs are almost always corporate entities rather than individuals, and landlord-tenant plaintiffs are often so.”9

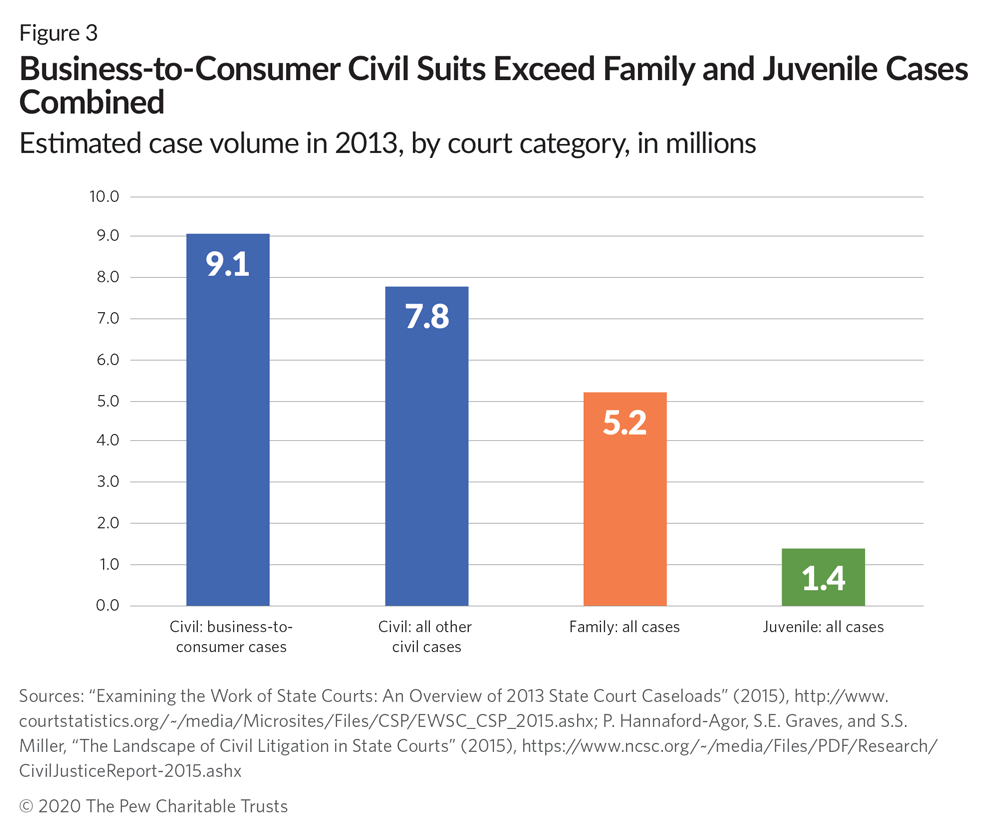

As of 2013, civil business-to-consumer lawsuits exceeded all court categories except traffic and criminal, and that same year, state courts heard more business-to-consumer cases than family (or “domestic relations”) and juvenile cases combined.10 (See Figure 3.)

Although organizing civil litigation cases into discrete categories can be useful for broad analytical purposes, determining exactly how many cases fall into each group is not so simple. For example, some landlord-tenant disputes involve individual landlords rather than companies, so a subset of cases within that category may not fall under the business-to-consumer umbrella. On the other hand, a large share of cases filed in small claims court are low-dollar-value business-to-consumer lawsuits, but because courts typically do not distinguish small claims by case type, the exact proportion is difficult to determine. Accordingly, Figures 2 and 3 almost certainly understate the share of civil court cases that involve businesses suing individual consumers because it treats small claims as a wholly separate category.

Debt claims increasingly dominated civil court dockets

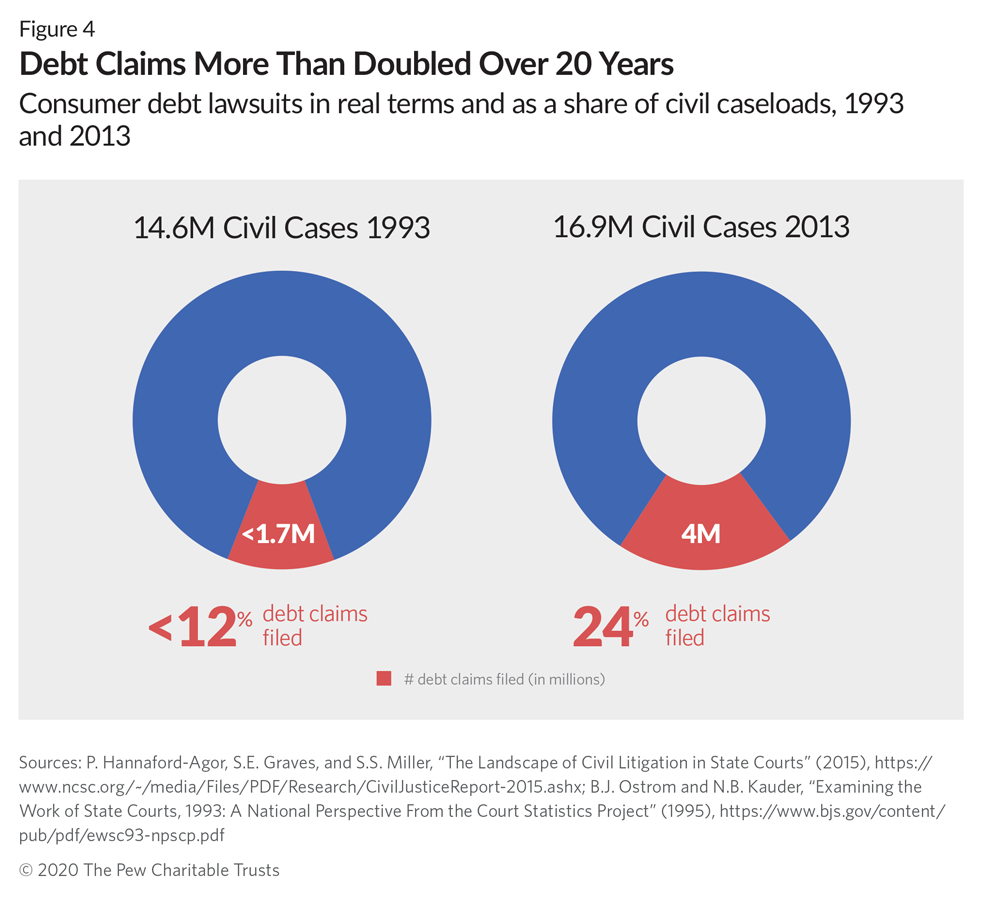

The most recent national data show that, as of 2013, debt collection lawsuits—which most often involve unpaid medical, auto loan, or credit card bills—have become the single most common type of civil litigation, representing 24 percent of civil cases compared with less than 12 percent two decades earlier.11 (See Figure 4.) From 1993 to 2013, the number of debt cases rose from fewer than 1.7 million to about 4 million.12 These figures correspond with an increase in share from an estimated 1 in 9 of 14.6 million state civil cases nationwide (11.6 percent) to about 1 in 4 of 16.9 million cases (23.6 percent)13. Further, in a national survey by the Consumer Financial Protection Bureau (CFPB), nearly 1 in 20 adults with a credit report reported having been sued by a creditor or debt collector in 2014.14

Notably, the 2013 data show that 75 percent of civil case judgments were for less than $5,200,15 which means that in most states, debt claims are typically filed in a limited or small claims court. In fact, NCSC observed in 2015 that small claims courts “have become the forum of choice for attorney-represented plaintiffs in lower-value debt collection cases.”16 As was the case for the business-to-consumer cases shown in Figure 3, the data in Figure 4 probably undercount debt claims because they do not include any debt collection cases filed in small claims court.

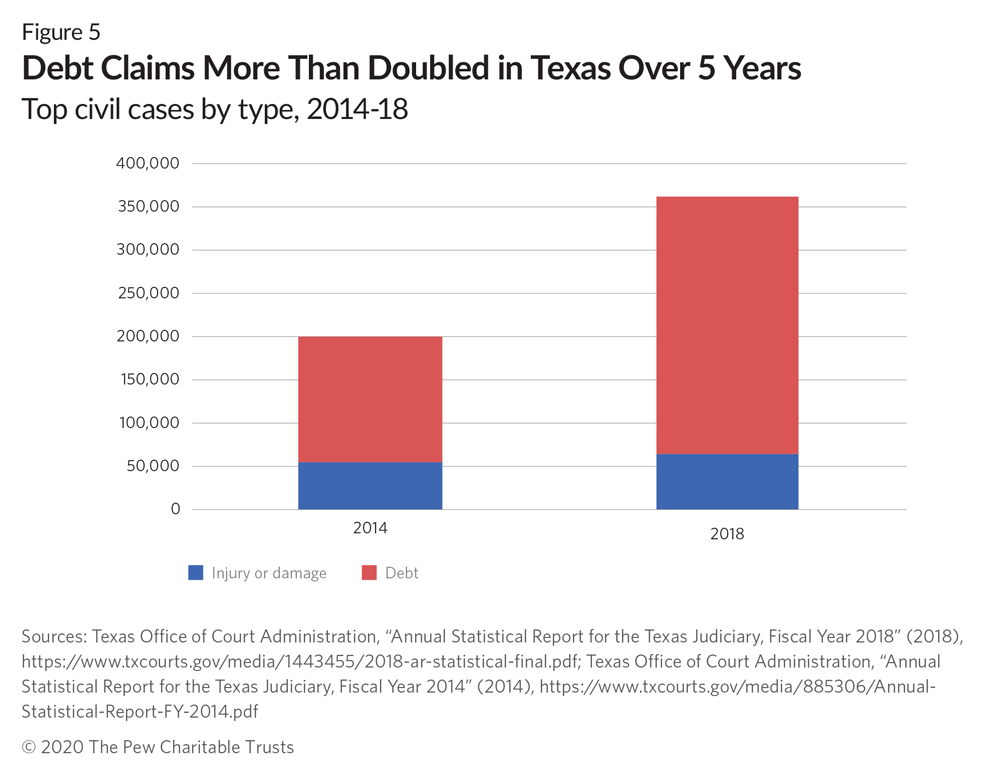

Only a few state courts have consistently reported data on debt claims since 2013, but the available information indicates that these lawsuits continue to dominate court dockets. For example, in 2018, the number of debt collection lawsuits filed across all Texas courts was more than twice what it was in 2014.17(See Figure 5.) The state’s small claims courts—known as justice courts—alone experienced a 140 percent increase in debt cases over that five-year period.18 In total, collectors filed one debt claim for every 19 adults in the state over that span.19

Similarly, Alaska’s District Court, which tries all civil matters in the state for values of $100,000 or less, heard 48 percent more debt claims in fiscal year 2018 than 2013.20

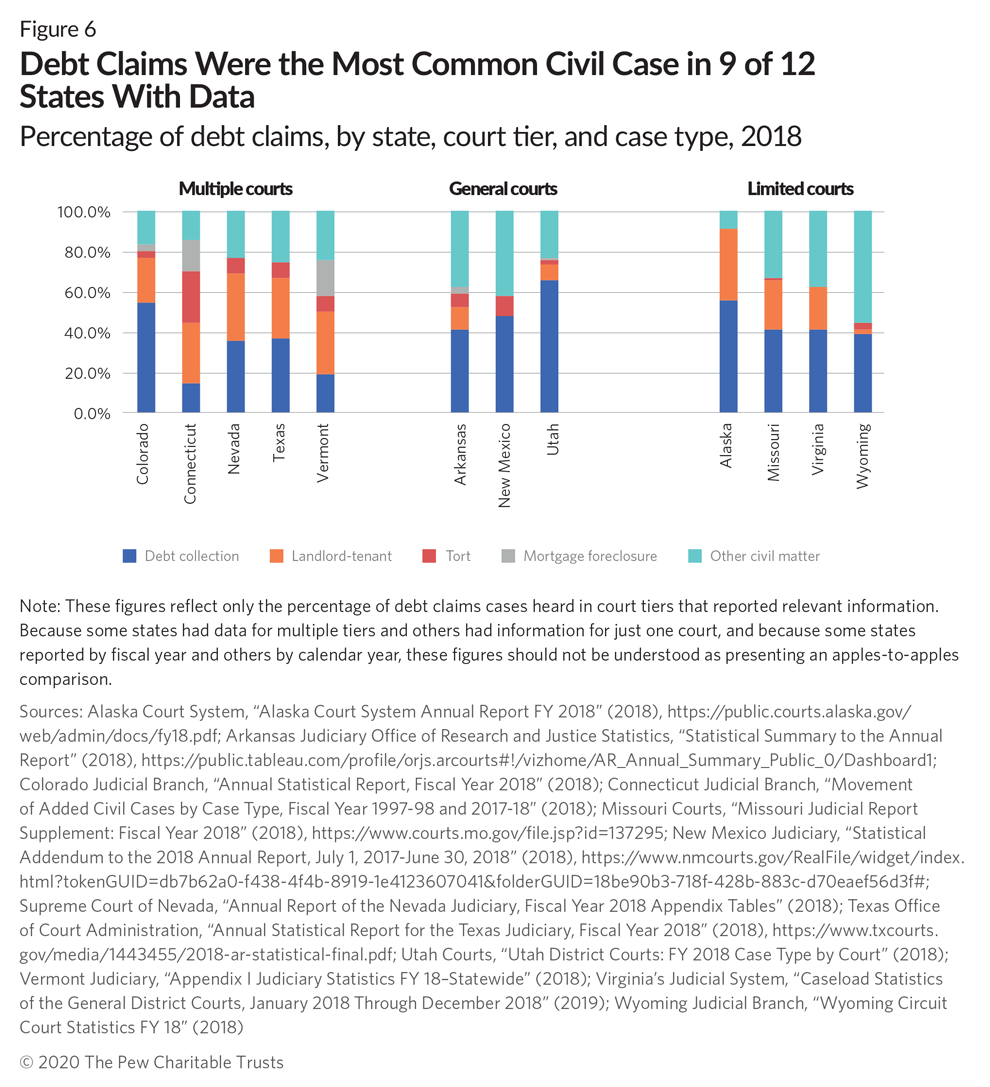

Pew found that in 2018, only 12 states—Alaska, Arkansas, Colorado, Connecticut, Missouri, Nevada, New Mexico, Texas, Utah, Vermont, Virginia, and Wyoming—reported statewide debt claims caseload data for at least one of their courts on their public websites.21 Virginia, for instance, reports debt claims data for the state’s district courts—which hear cases with values up to $25,000—but not the circuit courts, which hear cases with values of $4,500 and up.22 Despite these differences, debt claims are consistently among the most common types of cases in the courts that report relevant information. (See Figure 6.) However, in light of the limited number of states and courts reporting, more data and research are needed to gain a complete picture of what is happening nationwide and state by state.

Factors Contributing to the Rise of Debt Claims

The increase in debt claims parallels two major national trends: a rise in household debt and the emergence of the debt-buying industry.

Americans’ household debt nearly tripled from $4.6 trillion in 1999 to $12.29 trillion in 2016, roughly overlapping with the period of rapid growth in debt collection litigation.23 Further, as of 2018, an estimated 71 million people—nearly 32 percent of U.S. adults with a credit history—had debt in collections reported in their credit files, and 1 in 8 households across all income levels had a problem or dispute related to debt, credit, or loans.24

Most household debt in collection stems from a financial shock, such as a job loss, illness, or divorce, and reflects the broader financial fragility of many American households. Nationwide, 2 in 5 adults say that, without selling personal property or borrowing the money, they would not have enough cash to cover an emergency expense costing $400,25 and 1 in 3 families report having no savings.26 Medical debt can be particularly devastating and accounts for more than half of all collections activity.27

Unsurprisingly, low- and moderate-income Americans are disproportionately affected by debt collection. A 2017 CFPB survey found that people in the lowest income bracket were three times as likely as those in the highest income group to have been contacted about a debt in collection and that people with lower incomes also were more likely to have been sued for a debt.28

Creditors who pursue consumer debts into collection include banks and credit unions, hospitals and other medical providers, utility companies, telecommunications companies, auto and student lenders, and, increasingly, debt buyers—firms that purchase defaulted debts from the original creditors at a fraction of the face value, sometimes less than one cent on the dollar, and then attempt to collect on the full amount owed.29

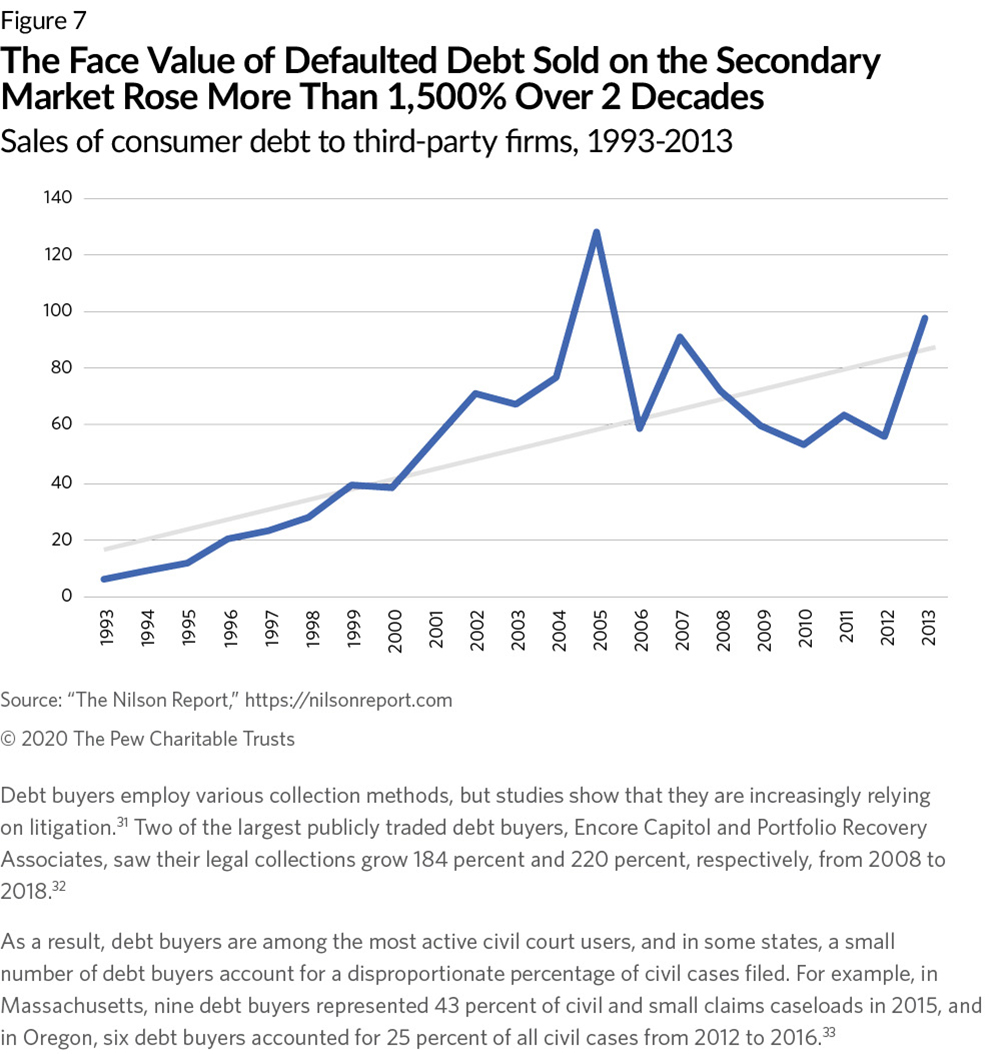

Debt buyers are key figures in many debt collection lawsuits and may have played a significant role in the rise of civil debt cases. During the same 20-year time frame that debt claims increased, 1993 to 2013, the total dollar value of debts purchased by debt buyers grew from $6 billion to $98 billion.30 (See Figure 7.)

Debt buyers employ various collection methods, but studies show that they are increasingly relying on litigation.31 Two of the largest publicly traded debt buyers, Encore Capitol and Portfolio Recovery Associates, saw their legal collections grow 184 percent and 220 percent, respectively, from 2008 to 2018.32

As a result, debt buyers are among the most active civil court users, and in some states, a small number of debt buyers account for a disproportionate percentage of civil cases filed. For example, in Massachusetts, nine debt buyers represented 43 percent of civil and small claims caseloads in 2015, and in Oregon, six debt buyers accounted for 25 percent of all civil cases from 2012 to 2016.33

Courts are not designed to respond to the realities of debt claims

Although civil court dockets have changed, the rules they operate on have largely stayed the same. Courts expect both parties to mount a case and present legal arguments so that the judge can make a decision based on the facts.

However, that is not how today’s debt collection lawsuits play out.

Debt claim defendants rarely have legal representation

The U.S. Constitution provides the right to an attorney for most criminal defendants regardless of ability to pay,34 but that right extends to people being sued in civil court only in very limited instances. Instead, civil case litigants on both sides must pay for their own representation, and data show that such representation is on the decline, especially for those being sued. NCSC found that from the 1990s to 2013, the share of general matters cases in which both sides had a lawyer dropped by more than half, from 96 percent to 45 percent.35

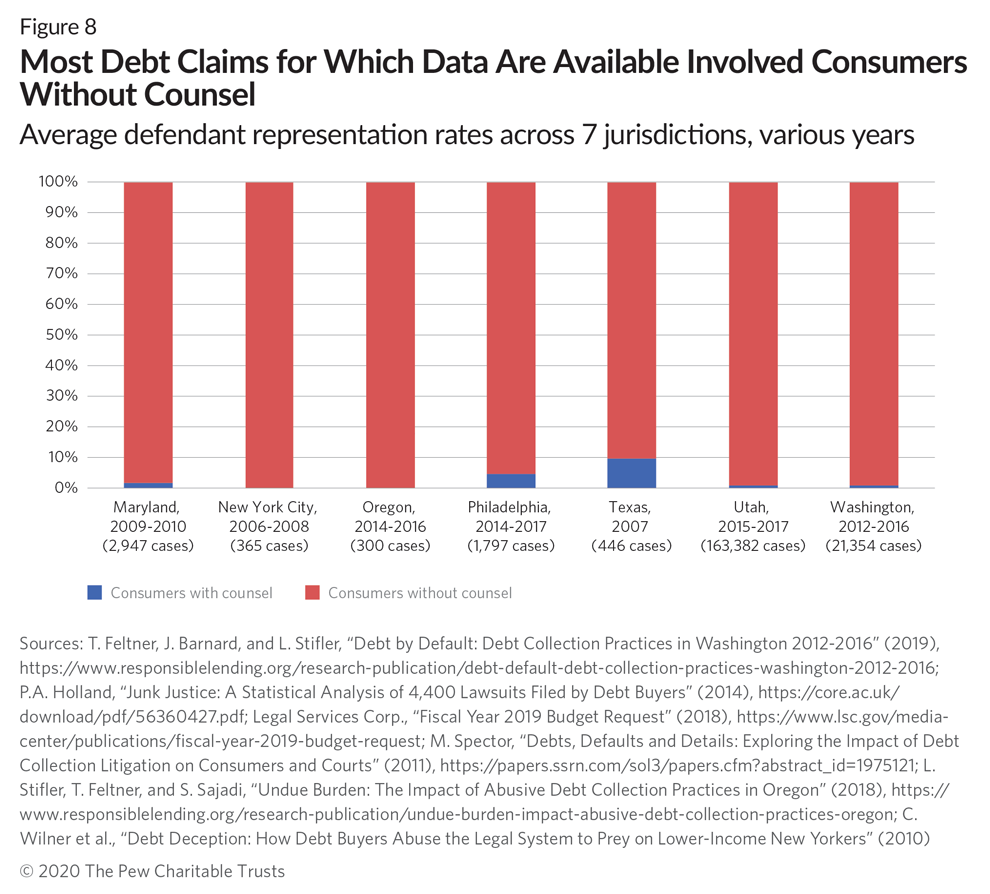

In business-to-consumer suits, and especially debt collection cases, most plaintiffs can afford an attorney, and filing multiple lawsuits in a single court can lower the cost per lawsuit filed. Consumers, however, typically have legal representation in less than 10 percent of debt claims. Studies from 2010 through 2019 show that the share of debt claim defendants who were served—that is, provided with official notification of the suit against them—who had an attorney ranged from 10 percent in Texas to zero in New York City.36 (See Figure 8.)

These low representation rates have real-world implications. Without representation, consumers are unlikely to know their full range of options or recognize opportunities to challenge the cases against them.

For example, every state has a statute of limitations for debt collection lawsuits, ranging from three years in Mississippi to 10 in Rhode Island.37 These laws create an expiration date after which creditors cannot use the courts to collect on a debt. However, enforcement of that prohibition typically falls on the defendant rather than on the courts. For example, if a plaintiff sues on such an expired debt, also called a time-barred debt, the defendant must raise the question of a statute of limitations in order for the court to consider whether the case is even eligible to be heard. But without professional legal help, most consumers would not have the requisite knowledge to demand that the plaintiff prove that the case was filed in time.

Of course, even defendants with representation may lose in court if the facts favor the plaintiff. However, analyses from jurisdictions across the country indicate that when consumers are represented by attorneys, they are more likely to secure a settlement or win the case outright.38 For example, a study of nearly 297,000 debt cases in Virginia district and circuit courts disposed between April 2015 and May 2016 found that debt cases were more likely to be dismissed if defendants were represented by an attorney.39 Similarly, a study of over 165,000 debt cases disposed in Utah from 2015 to 2017 found that 53 percent of represented defendants won their cases, compared with 19 percent of those without representation.40

These data indicate that the absence of legal counsel can have serious repercussions for defendants in consumer debt claims. The problem has become sufficiently widespread that in 2016, the Conference of Chief Justices (CCJ) and Conference of State Court Administrators’ (COSCA) Civil Justice Improvement Committee declared that lack of representation among defendants is “creating an asymmetry in legal expertise that, without effective court oversight, can easily result in unjust case outcomes.”41

Debt lawsuits frequently end in default judgment, indicating that many people do not respond when sued for a debt

Why do so few consumers in debt claims have lawyers? One reason is the prohibitive cost of a lawyer. But another, indicated by the outcome of large shares of debt collection cases, is that many consumers do not participate in the lawsuit at all.

Courts are designed to allow the opposing sides to present legal arguments and facts to support their positions, after which the judge, acting as a neutral arbiter, makes a decision based on that information.

What Are the Steps of a Debt Claim?

In most civil cases, the parties follow the state’s civil procedure:42

-

Plaintiff (e.g., creditor or debt buyer) files a complaint in court and provides notice of the lawsuit to defendant (i.e., person being sued).

-

Defendant responds with a written answer. If the defendant does not respond, the court issues a default judgment for the plaintiff.

-

The two parties exchange documents, including discovery (questions and requests for information) and pleadings (written motions and other legal maneuvers).

-

Court holds one or more hearings and possibly a trial. If a trial is held, parties can present evidence to a judge or jury.

-

Judge issues a ruling, which either party may appeal.

A judge presides over the hearings and possible trial, but the litigants manage nearly every step before that, and court processes, such as scheduling a hearing, are driven by their actions. Parties can also settle the case at any time by, for example, negotiating with each other or working with a neutral mediator.

For low dollar amounts, small claims courts use a different procedure, originally designed to provide streamlined and simplified proceedings, particularly for litigants without attorneys.43 Written answers are optional, rules of evidence do not apply, and in many jurisdictions, the parties have no immediate right to appeal. The common steps are:

-

Plaintiff files a complaint in court and notifies the defendant about the lawsuit.

-

Parties come to court for a trial in front of a magistrate or other judicial officer.

If one side doesn’t participate, however, the process cannot operate as intended. Judges do not independently evaluate the merit of a case before them; they rely on the defendant to argue that the case is invalid. With no defendant to argue, and regardless of the reason for the defendant’s failure to respond, court procedure dictates that the plaintiff wins automatically via a default judgment.44

And default judgments are alarmingly common in debt claims. Multiple studies have shown that more than 70 percent of debt cases end in default judgments:

-

In New York City, 4 in 5 cases filed from 2006 to 2008 resulted in a default judgment in favor of debt buyers.45

-

In five Colorado counties, 71 percent of collections lawsuits filed from 2013 to 2015 by debt buyers ended in default judgments for the plaintiffs.46

-

More than 80 percent of debt claims cases filed by debt buyers in Washington state’s superior court from January 2012 to December 2016 resulted in default judgments in favor of the plaintiffs.47

In these cases, the court has ruled in favor of the debt collector for the simple reason that the consumer has not participated in the case. Although the evidence on why people do not respond to the suits is scant, the available information suggests that three factors drive many of these instances: practical realities of consumers’ lives, unfamiliar plaintiffs, or a lack of notification about the suit.

Some consumers who owe a debt see no value in responding to a lawsuit. For example, the presiding judge of the Maricopa County (Arizona) Justice Courts has suggested that some defendants believe that their cause is futile and simply give up in the face of debts they cannot afford to pay.48 Some defendants may be intimidated or confused by the complexities of the system, while others might be daunted by the prospect of defending themselves if they cannot afford an attorney.49 One collections attorney observed that some defendants choose not to respond because they cannot afford to take off—or do not see the value in missing—work to go to court if they cannot afford to pay the debt, find child care, or secure transportation.50

Observational and interview data reveal that consumers often do not recognize the name of the company that filed the lawsuit. Debt buyers present a unique challenge in this regard because they are not the original lenders. Consumers frequently report not responding because they do not recognize the debt buyer suing them.51

Further, although some consumers may actively choose not to respond to debt claims, many are not aware that they are being sued. Some evidence, including interviews with civil court judges, suggests that inadequate notice is responsible for a meaningful share of instances in which defendants fail to respond to debt claims.52 Many states’ legal requirements regarding conducting service—the process of notifying defendants about a legal action against them—do not include any mechanism for ensuring that people are actually contacted.53 For example, in many jurisdictions, the plaintiff is responsible for serving the defendant with court papers but often only by first-class mail to the defendant’s last known address. Plaintiffs are typically not obligated to ensure that they have the correct address.

Further, in some debt claims cases, bad actors may employ faulty or fraudulent service as a litigation tactic. In California, Illinois, and New York, enforcement actions have been brought against debt claims plaintiffs for “sewer service”—a practice in which a process server knowingly fails to serve the defendant but attests to the court that service was made.54

In its 2010 report, the FTC urged states to adopt “measures to make it more likely that consumers will defend in litigation.”55 Although some states are taking action to ensure that defendants are properly informed of lawsuits against them, many continue to rely on plaintiffs to notify their opponents while providing little or no oversight.56

Whatever the reason for the consumer’s failure to appear, default judgment in debt claims usually means that the court makes no finding as to the validity of the debt, the accuracy of the amount sought,57 or whether the correct consumer was sued, but simply orders the defendant to pay the debt sought. As a result, debt collectors sometimes win cases that feature inaccurate information or are filed after the legal right to sue has expired.58And despite their lack of a factual or legal foundation, default judgments carry the same weight and enforcement power as any other court decision.

Racial Disparities in Debt Claims

Research indicates that debt collections and related lawsuits disproportionately affect African American and Hispanic communities.59 In a study in New York City, 95 percent of people with default debt claims judgments entered against them lived in low- or moderate-income neighborhoods, and more than half of those individuals lived in predominantly African American or Latino communities.60 A similar analysis of court judgments over a five-year period in St. Louis, Chicago, and Newark, New Jersey, found that even after accounting for income, the rate of default judgments in mostly black neighborhoods was nearly double that of mostly white ones.61

Default judgments can exact heavy tolls on consumers

Debt collection lawsuits that end in default judgment can have lasting consequences for consumers’ economic stability. Court and attorney fees can amount to hundreds of dollars, and consumers can face wage garnishment and liens or even civil arrest for failure to comply with court orders. Over the long term, these consequences can impede people’s ability to secure housing, credit, and employment.

"People don’t appreciate the impacts of a small claim judgment. If this is on your record, you’re not going to get a housing loan or a car loan, and it impacts other areas of your life. And all for a very small debt claim."

Peter Holland, consumer attorney MARYLAND

Excess costs

Once a default judgment is entered, the consumer typically owes more than the original debt.62 All 50 states and the District of Columbia allow courts to award debt collectors pre- and post-judgment interest—that is, interest on the money owed before the court judgment and on the judgment amount. The rates vary dramatically across states—from 1.5 percent in New Jersey to 12 percent a year in Massachusetts—and apply only in cases for which the state has not set or does not permit use of a contract rate, which is typically outlined in the terms for credit cards, loans, and other consumer debt products.63

Consumers who find themselves paying high interest rates on default judgments can face an even deeper cycle of debt. For instance, in 2014, a collector in Washington state won a judgment for a $9,861 medical debt. Although the defendant had paid roughly $8,500 by 2019, she still owed an additional $8,500 because of interest—Washington statute sets the post-judgment interest rate at 12 percent—and other costs.64

In many states, a default judgment can also require the consumer to bear court and collector’s attorney fees. For example, one study from Maryland found that on average, courts ordered defendants in debt collection cases to pay principal of $2,811, but court costs, plaintiff attorneys’ fees, and interest added $512—more than 18 percent of the principal—to the total judgment.65

Court-enforced collection

Default judgments grant debt collectors access to a range of legal channels to pursue the debt, including the ability to garnish consumers’ paychecks and bank accounts and to put liens on property. A 2017 study by Automatic Data Processing Inc., one of the nation’s largest payroll providers, found that 1 in 14 U.S. workers were having paychecks garnished, and that among workers earning $25,000 to $39,000 a year, debt collection was one of the most common reasons.66

Under federal law, debt collectors are entitled to seize no more than 25 percent of a consumer’s paycheck.67 States have discretion to limit collectors to even less than the federal cap, but rules vary widely. Four states—North Carolina, Pennsylvania, South Carolina, and Texas—generally prohibit the garnishment of wages to pay off consumer debts.68 In contrast, Alabama, Arkansas, Georgia, Idaho, Kansas, Kentucky, Louisiana, Maryland, Michigan, Mississippi, Montana, Ohio, Utah, and Wyoming offer no protections beyond the federal minimum.69

The seizure of money from a bank account can be even more devastating than wage garnishment because it is unrestricted in 16 states, potentially leaving consumers with empty accounts.70 In one study from Missouri, for example, of 13,000 bank accounts garnished by collectors in 2012, more than 7,500 were entirely drained because there was less money in the account than the consumer owed.71 Bank account garnishment can also circumvent wage garnishment caps, because once a paycheck is deposited into a bank account, it is no longer subject to the limits set by federal or state law, and all the money can be legally garnished.72

Moreover, state seizure protections tend to be infrequently adjusted for inflation or changing times. Pennsylvania’s exemption law, for example, protects sewing machines, a few other specific items, and up to $300 in additional property but leaves everything else available to debt collectors.73

Asset garnishments and property liens can cause significant financial stress, especially for people whose finances are already precarious, such as the one-third of Americans who report having no savings and the 51 percent of working adults living paycheck to paycheck.74 These seizures can prevent people from selling or refinancing a home, taking out a loan, or making payments on other bills, and they can last for years. In Missouri, for example, a judgment to garnish assets is valid for 10 years and can be renewed by court order.75

Despite efforts by policymakers to restrict debt-related seizures, a 2019 review by the National Consumer Law Center (NCLC) found that every state and the District of Columbia fell short of protecting enough income and savings to ensure that consumers facing court-enforced collections could still meet basic needs.76

Arrest and incarceration

In the most extreme circumstances, consumers can be arrested and even incarcerated as a result of a debt collection judgment. Although nationwide, state laws prohibit the jailing of individuals for inability to pay a debt, in 44 states, people can be held in contempt of court and subject to a civil arrest warrant, typically issued by the court at the plaintiff’s request, if they fail to appear in court for post-judgment hearings or to provide information related to their finances.77 Defendants can be incarcerated without access to an attorney or, in some cases, without even knowing a judgment was entered against them.

Such incarceration is relatively rare, but when it does occur, it can cause significant harm to consumers,most notably loss of wages and disruption in employment.78 In addition, the bond that people must pay to get out of jail can perpetuate the cycle of debt.79 For instance, an elderly married couple jailed in Maryland in 2014 for failing to appear in court over a housing-related debt of about $3,000 were ordered to pay a $2,900 cash bond—nearly doubling the underlying debt.80

A lack of readily available data obscures procedural problems and consumer harm

Although this research highlights key issues in debt collection lawsuits, the picture of the challenges and consequences remains incomplete because state court data are scarce.81 NCSC’s 2015 report remains the only national study of debt claims from the past 10 years, and despite a sample size of more than 925,000 cases from 152 courts in 10 urban counties, that study examined just 5 percent of state civil caseloads nationally.82

Pew identified 12 states with at least some courts that provide public data on debt claims, as described previously, but those reports are not sufficiently robust to document trends over time. Just seven states—Alaska, Colorado, Connecticut, New Mexico, Texas, Utah, and Wyoming—have tracked statewide debt claims caseloads since 2013, and only Texas reports on debt collection cases for all its courts.83 Further, only Texas and Colorado identify debt claims as a category within the general civil and small claims dockets in publicly available reports. In 2018, just New Mexico and Texas reported a cross section of cases and disposition types, including default judgments, for at least one court type,84 and Texas was the only state to publish the disposition (including default judgment rate) for debt claims at all dollar amounts and in all courts.

Even fewer states provide details about how debt claims cases are resolved.

Court systems have difficulty producing statewide reports in part because they are decentralized and fragmented and generally collect data only for their own administrative purposes.85 Without better data than are currently available, however, states and researchers cannot effectively evaluate whether debt claims are increasing, what might be driving that growth, and what the implications are for consumers.

In some states, however, the landscape of available data is beginning to change. Texas is still the clear leader in reporting, but other states, notably Arkansas, Nevada, and Virginia, have started including debt collection lawsuits in their annual reports. Nevada also includes a more detailed breakout of the types of debt involved in debt claims, such as payday loans and credit cards. This information can help policymakers and court officials understand whether courts are serving the public as intended and make informed decisions about how to best allocate resources to ensure that taxpayer investments are directed toward the areas of greatest need.

States are beginning to recognize and enact reforms to address the challenges of debt claims

In addition to tracking and reporting debt claims trends, more and more court officials are beginning to take steps to examine court processes and rethink how debt claims proceed. To date, this work has generally involved policy and practice reviews and system modernization through technology solutions. Although these efforts are generally still in the early stages of development, with little data on their effectiveness, they nevertheless present an opportunity to examine some initial attempts at reform.

Importantly, the potential benefits of these changes are not limited to debt claims. Rather, they point to opportunities to modify court operations and processes to improve experiences for court users on a range of issues and case types. Future Pew research will examine other challenges facing state civil courts and look at how these and other reforms might bolster access.

Reviews of state policies, rules, and common practices

To strengthen consumer protections in the processing of debt litigation, the FTC recommended that states require debt collectors to include more information in their complaints about the alleged debt, adopt measures to reduce the chance that collectors will sue for debts that are beyond the statute of limitations, and enact laws “to prevent the freezing of a specified amount in a bank account including funds exempt from garnishment.”86

States have begun to take steps to improve consumer protection—including those outlined in the FTC’s recommendation—particularly bolstering requirements for litigant notification, documentation of claim validity, and enforcement of statutes of limitation. (See Table 1.) These efforts represent promising first steps, but further research is needed to examine their effectiveness in improving court access.

New policies require courts to verify that all parties are notified about lawsuits and court dates

A few jurisdictions have begun to modify court rules to improve their notification requirements. Massachusetts changed its small claims court rules to require that plaintiffs in debt collection cases verify the addresses of defendants using reliable sources, such as municipal or motor vehicle records, and demonstrate to the court that they successfully served the case information to the correct address.87 New York City adopted a procedure that requires debt collection plaintiffs to provide the court with a stamped, unsealed envelope addressed to the defendant with a return address to the court. The envelope contains a standardized notice of the lawsuit, which the court mails.88 The court will not enter a default judgment if the Postal Service returns the notice as undeliverable.

In addition to confirming that all parties have been notified about the lawsuit, courts in some states have made small but important changes to ensure that consumers understand what the lawsuit is about. Because consumers sometimes believe that they either do not owe the debt or have already paid it or do not recognize the creditor or debt buyer that is suing them, Maryland strengthened its rules to require that pleadings include details about the underlying debt to help consumers more easily identify the debt, reduce confusion, and improve response rates.89

Additional documentation requirements oblige courts to ensure that debt claims are accurate and valid

Some states have acted to enhance the integrity of debt claims dispositions by requiring courts to examine the plaintiff’s case before issuing a judgment, regardless of whether the defendant is present. These states require that plaintiffs provide documentation as a matter of course rather than expecting defendants to ask plaintiffs to prove their cases.

Legislatures are leading these efforts in several states. North Carolina, for instance, passed a law in 2009 prohibiting courts from entering a default judgment unless the plaintiff provides “authenticated business records” that include the original account number and creditor, the amount of the original debt, an itemization of charges and fees claimed, and other information.90 And in California, debt buyers must provide specific evidence related to their ownership of a debt, the amount of the original debt, and the name of the original creditor.91

In addition, court leaders have begun to set rules that require proof of the validity of a debt, even if the defendant is not in court. As of 2018, 11 states—California, Colorado, Delaware, Maine, Maryland, Massachusetts, Minnesota, New York, North Carolina, Oregon, and Texas—mandated documentation by court rule or statute. And in a 2018 policy resolution, the CCJ and the COSCA urged members “to consider enacting rules requiring plaintiffs in debt collection cases to file documentation demonstrating their legal entitlement to the amounts they seek to collect before entry of any default judgment where state legislation or court rules do not currently require the filing of such documentation.”92

Debt buyers, as well as consumer advocates, back requiring additional documentation that a debt is owed. For example, the Receivables Management Association International, a debt buyer trade group, “supports uniform standards on account documentation provided that they serve a legitimate purpose and is information that originating creditors are required to maintain.”93

State laws enhance prohibition of judgments on time-barred debts

In May 2019, the CFPB proposed amendments to its rules that enforce the federal Fair Debt Collection Practices Act.94 The draft rules included a new provision stating that “a debt collector must not bring or threaten to bring a legal action against a consumer to collect a debt that the debt collector knows or should know is a time-barreddebt.” As described earlier, most states currently place the responsibility on the defendant to question whether a debt has expired,95 and it is unclear whether the proposed rule would authorize courts to review cases for timing compliance even if a consumer does not raise the defense.

In the absence of specific federal rules, however, state legislators have taken up the issue of time-barred debt. Oregon law, for instance, prohibits a debt collector from knowingly filing legal action on a time-barred debt.96 Debt industry representatives argue that suing on time-barred debt is already illegal and that plaintiffs do not knowingly file such lawsuits.97 However, court data and judicial oversight are needed to confirm these assertions and to ensure that courts are not ruling in favor of collectors on invalid claims.

Modernization of court-user interactions

Some states are investing resources to leverage technology and adapt court procedures to better support self-represented litigants and improve court accessibility, affordability, and participation. These efforts include modifying court forms, enhancing outreach to consumers, and adopting online tools that make legal information and basic court services more easily available to users.

Providing relevant timely procedural information to all parties

Clear, accessible procedural information has the potential to yield significant benefits to court users and court operations. For example, Harvard Law School’s Access to Justice Lab conducted a randomized control trial in partnership with the Boston Municipal Court and found that debt claim defendants who received mailings from the court participated in their lawsuits at twice the rate of people who received no information by mail.98

Courts in several states have undertaken modernization efforts, such as updating legal documents with easy-to-understand language; providing information in multiple languages; and using illustrations, videos, and other alternative formats.99 In Alaska, for example, courts have created a self-help debt collection case website, developed a variety of plain-language forms, solicited feedback from the legal community on the revised forms, and proposed changes to court rules to facilitate participation by litigants without lawyers100 in response to an internal analysis, which showed widespread problems with debt claim cases.101

Similarly, Collin County, Texas, Justice of the Peace Chuck Ruckel, who hears more debt claims than any other case type and estimated that up to 98 percent of defendants in those cases have no lawyer, said the most common question he receives is, “What should I do?” His court distributes a self-help packet, titled “When a Debt Claim Case Has Been Filed Against You” and produced by the Texas Court Training Center, that helps people understand the steps they need to take when being sued.102

One critical consideration for courts is whether the information they provide is not merely available but in fact helpful to users. In 2019, the CCJ and COSCA passed a resolution103 calling on courts to generate “documents, forms, and other information … that is clear, concise, and easily comprehensible to all court users” and to explore online services as well as written self-help. These tools, whether static written information, interactive online content, in-person guidance, or some combination of the three, must be useful and usable.104

Some courts incorporate technology as a tool

Research increasingly suggests that technology holds promise for improving legal information and consumer outreach.105 In particular, several states, such as Illinois, Maine, Michigan, and Ohio, have created online legal assistance portals that contain self-help tools including explanatory articles, answers to common questions, step-by-step instructions for resolving a legal issue, and automated “interviews” that help litigants clarify and address their legal issues and complete court forms.106 Some portals also provide links to lawyer referral services, self-help centers, legal aid programs, and other community resources.

In addition, some court systems have begun harnessing technology to enable remote litigant participation in legal processes, particularly through online dispute resolution (ODR), a tool already used in the private sector to resolve disagreements between consumers and online merchants. In the court context, ODR allows people to handle civil legal disputes without setting foot in a courtroom, and state and local leaders are increasingly looking to this approach to streamline people’s interactions with civil courts and help court staff better manage caseloads. Since early 2019, chief justices of the supreme courts in Hawaii, Iowa, Texas, and Utah have highlighted ODR as a key priority in their State of the Judiciary addresses.107

Some jurisdictions—such as West Valley City, Utah, and Franklin County, Ohio—have begun using ODR for small debt claims in part to reduce the time that cases take to resolve.108 However, moving debt collection cases online is not a panacea. Without recognized best practices, some experts say, ODR could present its own risks for consumers. Lisa Stifler of the Center for Responsible Lending noted that “ODR has the potential to offer avenues to consumers to respond to lawsuits against them, but there are concerns about consumers unknowingly waiving rights or legal claims or defenses.”109

To address such concerns, the NCLC put out guidance for courts to consider when moving debt cases online.110 Additionally, as part of its upcoming research agenda, Pew plans to conduct evaluations of this technology to assess the risks and benefits for courts and ODR users.

Conclusion

From 1993 to 2013, the number of debt claims filed in civil courts across the country increased to the point of becoming the single largest share of civil court business over that span, particularly as people used civil courts less for other issues. The analysis underpinning this report found that, as a category, debt claims have largely one-sided outcomes, raising troubling questions about legal proceedings and case dispositions. It also revealed gaps in the available data as well as other topics that would benefit from additional research, such as why fewer people are using civil courts than in the past and whether technology and policy changes intended to modernize court systems are delivering the desired results.

This report examined early efforts in a handful of states to address these questions and challenges and identified three initial steps that state and local government officials can take to mitigate the challenges associated with debt claims and other business-to-consumer cases: Increase the collection and reporting of debt claim data; revise policies and rules; and update civil legal system processes, particularly through the use of technology, to make the system easier to navigate for people without attorneys.

However, these potential state actions, while important and necessary, amount only to a preliminary effort to make the civil legal system more accessible because the issues facing civil courts are long-term and far-reaching. For instance, court leaders, the legal community, and advocates have for years been raising concerns that the civil legal system is failing not only people sued for a debt but also people facing eviction, navigating child custody issues, pursuing a divorce, seeking a protective order, or dealing with some other event with life-changing consequences. This report aims to expand the conversation among policymakers at all levels of government about modernizing the civil legal system to better serve all of its users.

Appendix: Methodology

This study took a three-step approach to analyzing debt collection lawsuit trends in state courts and their impact on consumers. To identify common characteristics and consequences of these cases, Pew researchers conducted a literature review of peer-reviewed and gray studies and semistructured interviews with subject-matter experts. To analyze the volume of debt claims in the U.S. and the extent to which courts track relevant data, researchers reviewed annual court statistical reports in all 50 states and the District of Columbia. Pew researchers conducted quality control for each step to minimize errors and bias.

Literature review

Pew researchers conducted a literature review of consumer debt and debt collection lawsuits in the U.S. using keyword searches via four search engines—EBSCO, Hein Online, Google, and Google Scholar—to identify research related to debt collection lawsuits. Search terms included but were not limited to: “debt claim,” “debt collection lawsuit,” “debt litigation,” and “debt collection data.” Researchers also reviewed studies available on the websites of 24 organizations with a focus on debt collection or debt claims lawsuits. These searches generated approximately 130 apparently relevant articles, of which roughly 70 were found to contain information applicable to this study. The researchers examined and coded each article to identify common characteristics and themes in debt collection lawsuits.

Expert interviews

To collect additional insight on debt claims characteristics and consequences, Pew researchers performed semistructured interviews with three court officials, five consumer advocates and academics, and three credit lenders and debt collection attorneys.

Court data analysis

To identify the proportion of civil cases that were debt claims in 1993 and 2013, Pew researchers used data reported in two studies conducted by NCSC.111 Although the studies contained different sample courts, based on geographic diversity and other characteristics, NCSC considered each to be nationally representative. NCSC found that across all state courts, 64 percent of 16.9 million civil cases are contract disputes and that contract caseloads consisted primarily of debt collection (37 percent), landlord-tenant (29 percent), and foreclosure (17 percent) cases. Pew researchers calculated that debt collection lawsuits represented approximately 24 percent of the civil caseload (0.37 × 0.64 = 0.236), or 3.98 million cases (16.9 million × .236), which is higher than the other aggregated case types.

NCSC’s 1993 study reported 14.6 million civil cases in state courts, of which 8.6 million were filed in limited jurisdiction courts. In general jurisdiction courts, contracts accounted for 18 percent (or 1.08 million) of the 6 million general jurisdiction cases and 7 percent (or 602,000) of the 8.6 million limited jurisdiction cases. Contracts therefore made up 11.5 percent (1.08 million + 0.602 million/14.6 million) of the civil caseload. Debt collection was certainly less than 100 percent of the contract caseload. Both 1993 and 2013 figures are underestimated, as a significant percentage of small claims are also debt collection cases but are not counted in the contract caseloads.

Pew researchers used data collected by the NCSC Court Statistics Project (CSP) to analyze changes in state civil caseloads from 2009 to 2017. Idaho, Illinois, Mississippi, New Mexico, and Oklahoma did not report civil court data to CSP in 2017. A total of 40 states, as well as the District of Columbia and Puerto Rico, reported decreases in total civil filings from 2009 to 2017. Forty-three states, plus the District of Columbia and Puerto Rico, reported a decrease in civil filings per capita. Hawaii, North Dakota, and South Carolina reported increases in total civil filings but decreases in filings per capita. And the only states to report increases in total and per capita civil filings were Pennsylvania and Texas.

To identify debt claims reporting trends, Pew researchers searched state court websites for annual statistical reports. These reports are called by various names—e.g., annual report, court statistical report, court caseload report, etc.—and commonly include civil court data. Where available, researchers gathered and reviewed reports for calendar or fiscal years 2005, 2009, 2013, 2017, and 2018. Through this process, Pew was able to collect civil court data for 49 states and the District of Columbia, though the availability of data for each fiscal or calendar year varied. For Iowa, the court administrator’s staff provided the reporting that is shared with the state Legislature and bar association.

Table A.1

49 States and D.C. Provide Court Statistics Reports Online, Though Available Years Vary

Data websites by state

Sources: “National Center for State Courts AOC State Links,” https://www.ncsc.org/Topics/Court-Management/Administrative-Offices-of-the-Courts/State-Links.aspx; The Pew Charitable Trusts internal review of state court websites.

Next, the researchers reviewed the civil court data in each identified source and documented information related to:

-

Civil case filings and outcomes, particularly whether the data were disaggregated by case type.

-

Types of civil cases reported.

-

Small claims filings and outcomes.

-

Debt claims filings and outcomes.

-

Definitions of small claims and debt claims.

If a source did not contain the information sought, the research team searched for other public sources on courts’ websites that may include this information—e.g., a data dashboard, etc., using the phrases “civil case data,” “caseload statistics,” or “caseload data.” To ensure that all relevant sources of publicly available court data were examined, the team also contacted court administration offices in all 50 states and the District of Columbia.

Next, the researchers compiled three simple descriptive statistics to assess reporting trends:

-

The number of states that disaggregate their filings and outcomes information by case type.

-

The number of states that include debt claims as a subcategory within one or more tiers or dollar thresholds of civil cases (small claims, limited civil, general civil).

-

The number of states that report on the number of self-represented litigants.

To identify small and debt claims filings and outcomes trends, researchers collected data from the state reports identified above for years 2005, 2009, 2013, 2017, and 2018 and documented the following information (where available):

-

Small claims maximum limit.

-

Small claims caseload and default judgments.

-

Debt claims caseload and default judgments.

Pew researchers were unable to find publicly accessible reports for the following years and states as of October 2019:

-

2005: Georgia, Iowa, Kentucky, Nebraska, Oklahoma, Vermont, West Virginia, Wyoming.

-

2009: Iowa, Kentucky, Oklahoma, Vermont.

-

2013: Iowa.

-

2017: Idaho, Iowa.

-

2018: Arkansas (labeled 2018 annual report but reporting on 2017 data), Idaho, Illinois, Iowa.

In addition, 20 states and the District of Columbia report their data on a calendar year basis, while 29 do so on a fiscal year.

-

Calendar year states: Arkansas, District of Columbia, Illinois, Indiana, Kentucky, Louisiana, Michigan, Minnesota, Montana, New Hampshire, New York, North Dakota, Ohio, Oregon, Pennsylvania, Rhode Island, Virginia, Washington, West Virginia, Wisconsin, Wyoming.

-

Fiscal year states: Alabama, Alaska, Arizona, California, Colorado, Connecticut, Delaware, Florida, Georgia, Hawaii, Idaho, Kansas, Maine, Maryland, Massachusetts, Mississippi, Missouri, Nebraska, Nevada, New Jersey, New Mexico, North Carolina, Oklahoma, South Carolina, South Dakota, Tennessee, Texas, Utah, and Vermont.

-

Iowa does not produce public reports.

Where available, the research team performed descriptive analyses of small claims and debt claims trends from fiscal 2005 to fiscal 2018 to assess:

-

Differences in filings, including per capita, and default judgment rates.

-

Small claims caseload as a percentage of total civil caseload.

-

Debt claims caseload as a percentage of small claims caseload.

Limitations

Several factors can contribute to small claims and debt claims trends in each jurisdiction, such as the maximum dollar amount a plaintiff can sue for in a small claims court, rules and regulations governing the evidence required to file a debt collection lawsuit, the statute of limitations, filing fees, or the availability of electronic filing. Because of timing and resource constraints, assessing all these factors across the states and the District of Columbia was beyond the scope of this analysis. But this study was able to identify which of the six states that reported some information about debt claims caseloads in 2013 or earlier had also experienced a change in rules or court proceedings specifically targeting debt claims.

Endnotes

-

Federal Trade Commission, “Repairing a Broken System: Protecting Consumers in Debt Collection Litigation and Arbitration” (2010), https://www.ftc.gov/sites/default/files/documents/reports/federal-trade-commission-bureau-consumer-protection-staff-report-repairing-broken-system-protecting/debtcollectionreport.pdf.

-

National Center for State Courts, “State Court Statistics, 1985-2001: United States” (Inter-University Consortium for Political and Social Research, 2005); K. Genthon, senior court research analyst, Court Statistics Project, National Center for State Courts, email to The Pew Charitable Trusts, Sept. 5, 2019.

-

Genthon, email. Due to differences in reporting, the National Center for State Courts is unable to demonstrate adjusted caseload data pre- and post-2003 to enable them to be charted together. However, NCSC has consistently reported a general upward trend from the 1980s to 2003.

-

Court Statistics Project, “State Court Caseload Digest, 2017 Data” (Conference of State Court Administrators and National Center for State Courts, 2019), http://www.courtstatistics.org/~/media/Microsites/Files/CSP/Overview/CSP Caseload Digest 2017 Data print.ashx; National Center for State Courts, “State Court Statistics, 2009” (2012), https://www.icpsr.umich.edu/icpsrweb/NACJD/series/80.

-

E. Rickard, “Many U.S. Families Faced Civil Legal Issues in 2018” (The Pew Charitable Trusts, 2019), https://www.pewtrusts.org/en/research-and-analysis/articles/2019/11/19/many-us-families-faced-civil-legal-issues-in-2018.

-

For example, cases involving civil asset forfeiture, in which prosecutors file a lawsuit in civil court to keep property (e.g., car or money) that was allegedly used or seized in a crime.

-

National Center for State Courts, “Civil Jurisdiction Thresholds” (2015), https://www.ncsc.org/~/media/Files/PDF/Topics/Civil%20Procedure/Civil%20Jurisdiction%20Thresholds%20History.ashx.

-

P. Hannaford-Agor, S.E. Graves, and S.S. Miller, “The Landscape of Civil Litigation in State Courts” (National Center for State Courts, 2015), https://www.ncsc.org/~/media/Files/PDF/Research/CivilJusticeReport-2015.ashx. Notably, debt collection lawsuits are not resolved by arbitration, so even if certain types of cases are leaving the courts, debt collection is probably not one of them. In 2009, the Minnesota attorney general brought a federal lawsuit against a private arbitration company for colluding with creditors to collect on debts, and as a result, private arbitration companies have declared a moratorium on providing their arbitration services for debt collectors pursuing debts. See: American Arbitration Association, “Notice on Consumer Debt Collection Arbitrations,” http://www.adr.org; Consumer Financial Protection Bureau, “Arbitration Study: Report to Congress, Pursuant to Dodd-Frank Wall Street Reform and Consumer Protection Act § 1028(a)” (2015), http://purl.fdlp.gov/GPO/gpo57021; State v. National Arbitration Forum (Minn. Dist. Ct. Hennepin Cty., July 17, 2009).

-

National Center for State Courts, “Appendix I: Problems and Recommendations for High-Volume Dockets” (2016), https://www.ncsc.org/~/media/Microsites/Files/Civil-Justice/NCSC-CJI-Appendices-I.ashx.

-

Court Statistics Project, “Examining the Work of State Courts: An Overview of 2013 State Court Caseloads” (2015), http://www.courtstatistics.org/~/media/Microsites/Files/CSP/EWSC_CSP_2015.ashx; Hannaford-Agor, Graves, and Miller, “The Landscape of Civil Litigation.”

-

Hannaford-Agor, Graves, and Miller, “The Landscape of Civil Litigation”; B.J. Ostrom and N.B. Kauder, “Examining the Work of State Courts, 1993: A National Perspective From the Court Statistics Project” (Court Statistics Project, 1995), https://www.bjs.gov/content/pub/pdf/ewsc93-npscp.pdf; National Center for State Courts, “Call to Action: Achieving Civil Justice for All” (2016), https://www.ncsc.org/~/media/microsites/files/civil-justice/ncsc-cji-report-web.ashx. See the appendix for details on how Pew researchers identified these findings.

-

Hannaford-Agor, Graves, and Miller, “The Landscape of Civil Litigation”; Ostrom and Kauder, “Examining the Work of State Courts, 1993.” See the appendix for more information on how Pew estimated the debt claims caseloads in 1993 and 2013.

-

Hannaford-Agor, Graves, and Miller, “The Landscape of Civil Litigation”; Ostrom and Kauder, “Examining the Work of State Courts, 1993.”

-

Consumer Financial Protection Bureau, “Consumer Experiences With Debt Collection: Findings From the CFPB’s Survey of Consumer Views on Debt” (2017), https://files.consumerfinance.gov/f/documents/201701_cfpb_Debt-Collection-Survey-Report.pdf. Pew researchers estimated this figure using data from the study.

-

Hannaford-Agor, Graves, and Miller, “The Landscape of Civil Litigation.”

-

Ibid., 33. “… it raises troubling concerns that small claims courts, which were originally developed as a forum in which primarily self-represented litigants could use a simplified process to resolve civil cases quickly and fairly, provide a much less evenly balanced playing field than was originally intended.”

-

Texas Office of Court Administration, “Annual Statistical Report for the Texas Judiciary, Fiscal Year 2018” (2018), https://www.txcourts.gov/media/1443455/2018-ar-statistical-final.pdf.

-

Ibid.

-

Ibid. Pew researchers estimated this figure using data from the report.

-

Alaska Court System, “Alaska Court System Annual Report FY 2013” (2014); Alaska Court System, “Alaska Court System Annual Report FY 2018” (2018), https://public.courts.alaska.gov/web/admin/docs/fy18.pdf.

-

This analysis is based on states that report the required information on the court’s website. Some states may track this data but not report it on the website. See the appendix for the list of court websites used in this study.

-

Virginia’s Judicial System, “Caseload Statistics of the General District Courts, January 2018 Through December 2018” (2019); Virginia’s Judicial System, “Virginia Courts in Brief” (2019), http://www.courts.state.va.us/courts/cib.pdf; Virginia’s Judicial System, “PLN-GCMS 10.01 Caseload Statistics of the General District Courts, January 2018 Through December 2018 Filings” (2018), http://www.courts.state.va.us/courtadmin/aoc/judpln/csi/home.html.

-

Federal Reserve Bank of New York, “Quarterly Report on Household Debt and Credit” (2010), https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/DistrictReport_Q22010.pdf; Federal Reserve Bank of New York, “Quarterly Report on Household Debt and Credit” (2016), https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/HHDC_2016Q2.pdf.

-

Urban Institute, “71 Million U.S. Adults Have Debts in Collection” (2018), https://www.urban.org/urban-wire/71-million-us-adults-have-debt-collections; Rickard, “Many U.S. Families Faced Civil Legal Issues in 2018.”

-

B. Adler, B. Polak, and A. Schwartz, “Regulating Consumer Bankruptcy: A Theoretical Inquiry,” The Journal of Legal Studies 29, no. 2 (2000): 585-613; Board of Governors of the Federal Reserve System, “Report on the Economic Well-Being of U.S. Households in 2017” (2018), https://www.federalreserve.gov/publications/files/2017-report-economic-well-being-us-households-201805.pdf; J.M. Collins, “Exploring the Design of Financial Counseling for Mortgage Borrowers in Default,” Journal of Family and Economic Issues 28, no. 2 (2007): 207-26; C.E. Herbert, Report to Congress on the Root Causes of the Mortgage Foreclosure Crisis (2010).

-

The Pew Charitable Trusts, “What Resources Do Families Have for Financial Emergencies?” (2015), https://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2015/11/emergency-savings-what-resources-do-families-have-for-financial-emergencies.

-

Consumer Financial Protection Bureau, “Consumer Credit Reports: A Study of Medical and Non-Medical Collections” (2014), https://files.consumerfinance.gov/f/201412_cfpb_reports_consumer-credit-medical-and-non-medical-collections.pdf.

-

Consumer Financial Protection Bureau, “Consumer Experiences With Debt Collection.”

-

Federal Trade Commission, “The Structure and Practices of the Debt Buying Industry” (2013), https://www.ftc.gov/sites/default/files/documents/reports/structure-and-practices-debt-buying-industry/debtbuyingreport.pdf; Consumer Financial Protection Bureau, “Market Snapshot: Online Debt Sales” (2017), https://www.consumerfinance.gov/documents/2249/201701_cfpb_Online-Debt-Sales-Report.pdf.

-

R.J. Hobbs and C.L. Carter, Fair Debt Collection (National Consumer Law Center, 2008). Ch. 1.3.4.2, citing The Nilson Report: Issues 792 (July 2003); 806 (March 2004); 835 (June 2005); 857 (May 2006); 880 (May 2007); 901 (April 2008); 921 (March 2009); 946 (April 2010); 969 (April 2011); 992 (April 2012); 1019 (June 2013); 1041 (May 2014).

-

C. Albin-Lackey, “Rubber Stamp Justice: US Courts, Debt Buying Corporations, and the Poor” (Human Rights Watch, 2016), https://www.hrw.org/sites/default/files/report_pdf/us0116_web.pdf; P. Kiel, “So Sue Them: What We’ve Learned About the Debt Collection Lawsuit Machine,” ProPublica, May 5, 2016, https://www.propublica.org/article/so-sue-them-what-weve-learned-about-the-debt-collection-lawsuit-machine; A. Kuehnhoff and M. Best (staff attorneys at the National Consumer Law Center), testimony before the Joint Financial Services Committee (May 2, 2019), https://www.nclc.org/images/pdf/debt_collection/testimony-debt-collection-may2019.pdf; L. Stifler, T. Feltner, and S. Sajadi, “Undue Burden: The Impact of Abusive Debt Collection Practices in Oregon” (Center for Responsible Lending, 2018), https://www.responsiblelending.org/research-publication/undue-burden-impact-abusive-debt-collection-practices-oregon.

-

Encore Capital Group Inc., “Form 10-K, 2008” (2009), https://investors.encorecapital.com/financial-information/annual-reports; Encore Capital Group Inc., “Form 10-K, 2018” (2019), https://investors.encorecapital.com/financial-information/annual-reports; PRA Group Inc., “Form 10-K, 2008” (2009), https://ir.pragroup.com/sec-filings; PRA Group Inc., “Form 10-K, 2018” (2019), https://ir.pragroup.com/sec-filings.

-

Kuehnhoff and Best, testimony; Stifler, Feltner, and Sajadi, “Undue Burden.”

-

Scott v. Illinois, 440 U.S. 367 (1979); Gideon v. Wainwright, 372 U.S. 335 (1963).

-

Hannaford-Agor, Graves, and Miller, “The Landscape of Civil Litigation.”

-

T. Feltner, J. Barnard, and L. Stifler, “Debt by Default: Debt Collection Practices in Washington 2012-2016” (Center for Responsible Lending, 2019), https://www.responsiblelending.org/research-publication/debt-default-debt-collection-practices-washington-2012-2016; Stifler, Feltner, and Sajadi, “Undue Burden”; C. Wilner et al., “Debt Deception: How Debt Buyers Abuse the Legal System to Prey on Lower-Income New Yorkers” (New Economy Project, Legal Aid Society, MFY Legal Services, and Urban Justice Center, 2010); Legal Services Corp., “Fiscal Year 2019 Budget Request” (2018), 9-10, https://www.lsc.gov/media-center/publications/fiscal-year-2019-budget-request; P.A. Holland, “Junk Justice: A Statistical Analysis of 4,400 Lawsuits Filed by Debt Buyers,” Loyola Consumer Law Review 26, no. 2 (2014): 179-246, https://core.ac.uk/download/pdf/56360427.pdf; M. Spector, “Debts, Defaults and Details: Exploring the Impact of Debt Collection Litigation on Consumers and Courts,” Virginia Law & Business Review 6, no. 2 (2011): 257, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1975121. This problem is part of a larger trend in civil litigation nationwide. The NCSC found that attorney representation among defendants declined dramatically across all civil cases from 1992 to 2013, falling from 97 percent to 46 percent in general jurisdiction cases over that span. See: Hannaford-Agor, Graves, and Miller, “The Landscape of Civil Litigation,” 31.

-

Federal Trade Commission, “Time-Barred Debts,” accessed Jan. 22, 2020, https://www.consumer.ftc.gov/articles/0117-time-barred-debts; Rhode Island Gen. Law § 9-1-13; Mississippi Code § 75-3-118.

-

Holland, “Junk Justice.” One Maryland study of lawsuits in which defendants had pro bono legal counsel showed that debt buyers obtained monetary judgments in only 15 percent of those cases.

-

National Center for State Courts, “Virginia Self-Represented Litigant Study: Outcomes of Civil Cases in General District Court, Juvenile & Domestic Relations Court, and Circuit Court” (2017), https://ncsc.contentdm.oclc.org/digital/collection/accessfair/id/810.

-

Legal Services Corp., “Fiscal Year 2019 Budget Request,” 10.

-

National Center for State Courts, “Call to Action.”

-

American Bar Association, “Steps in a Trial,” accessed Feb. 3, 2020, https://www.americanbar.org/groups/public_education/resources/law_related_education_network/how_courts_work/steps_in_a_trial2/.

-

B. Yngvesson and P. Hennessey, “Small Claims, Complex Disputes: A Review of the Small Claims Literature,” Law & Society Review 9, no. 2 (1975): 219-74, http://doi.org/10.2307/3052976.

-

See for example, Albin-Lackey, “Rubber Stamp Justice”; Legal Services Corp., “Fiscal Year 2019 Budget Request”; Feltner, Barnard, and Stifler, “Debt by Default”; J. Fox, “Do We Have a Debt Collection Crisis? Some Cautionary Tales of Debt Collection in Indiana,” Loyola Consumer Law Review 24 (2011): 355; Holland, “Junk Justice”; M. Spector and A. Baddour, “Collection Texas-Style: An Analysis of Consumer Collection Practices in and out of the Courts,” Hastings Law Journal 67 (2015): 1427; Stifler, Feltner, and Sajadi, “Undue Burden.” In 2015, the NCSC found that fewer than 5 percent of cases were adjudicated on the merits of the case. See: Hannaford-Agor, Graves, and Miller, “The Landscape of Civil Litigation.”

-

Wilner et al., “Debt Deception.”

-

E. Harnick, L. Stifler, and S. Sajadi, “Debt Buyers Hound Coloradans in Court for Debts They May Not Owe” (Center for Responsible Lending, 2016), https://www.responsiblelending.org/research-publication/debt-buyers-hound-coloradans-court-debts-they-may-not-owe.

-

Feltner, Barnard, and Stifler, “Debt by Default.”

-

Albin-Lackey, “Rubber Stamp Justice.”

-

R.W. Staudt and P.L. Hannaford, “Access to Justice for the Self-Represented Litigant: An Interdisciplinary Investigation by Designers and Lawyers,” Syracuse Law Review 52 (2002): 1017.5

-

C. Brugnoli (attorney, Brugnoli Law Firm), interview with The Pew Charitable Trusts, June 11, 2019.

-

Federal Trade Commission, “Repairing a Broken System.”

-

New York Appleseed and Jones Day, “Due Process and Consumer Debt: Eliminating Barriers to Justice in Consumer Credit Cases” (2010), https://www.ftc.gov/sites/default/files/documents/public_comments/protecting-consumers-debt-collection-litigation-and-arbitration-series-roundtable-discussions-august/545921-00031.pdf; Federal Trade Commission, “Repairing a Broken System”; Albin-Lackey, “Rubber Stamp Justice.”

-

National Association of Professional Process Servers, “Civil Rules Guide for All 50 United States and the District of Columbia” (2017), https://www.sheriffs.org/sites/default/files/Civil%20Rules%20Guide%202017%20Redux.pdf.

-

See lawsuits against debt collectors for fraudulent service, in J.K. Steinberg, “A Theory of Civil Problem-Solving Courts,” NYU Law Review 93 (2018): 1579.

-

Federal Trade Commission, “Repairing a Broken System.”

-

Albin-Lackey, “Rubber Stamp Justice.”

-